{kind=link}

A number of states have not too long ago capped shopper mortgage charges with the said objective of defending debtors. In a latest Employees Report, we examine how these interventions have performed out in three states. In our first publish about that examine, we confirmed that price caps lead riskier debtors to face rationing within the credit score market. One query that naturally arises is what lenders do with the credit score they used to offer to high-risk debtors earlier than the caps had been imposed. Lenders that lend completely to high-risk debtors (at charges above the cap) could determine to cease lending to high-risk debtors in that state. Others, nonetheless, could attempt to change their “credit score field” by lending extra to considerably safer debtors. On this publish, we’ll attempt to perceive how lenders reallocate credit score after usury limits are carried out.

Rationing versus Re-allocation

Whereas credit score rationing below usury limits is clearly predicted by textbook financial principle, reallocation is much less apparent. In any case, if lending extra to safer debtors is worthwhile with a price cap, why not achieve this with out a cap? Primarily based on the straightforward mannequin supplied within the final publish, price caps on high-risk debtors shouldn’t have an effect on debtors with larger danger scores which have entry to conventional credit score markets. Nevertheless, lenders could not have the ability to lend to each high-risk and low-risk debtors resulting from restricted entry to capital, and a few will discover it extra worthwhile to focus on high-risk debtors. When the usury limits are put in place, lenders who had beforehand chosen to give attention to high-risk debtors could reallocate their capital to safer debtors.

Some current theoretical work helps this view. As an example, an early evaluation by Blitz and Lang (1965) exhibits that below sure circumstances, lenders will reallocate credit score to moderate-risk debtors when going through a usury restrict: “it’s the much less dangerous debtors…who’re most certainly to learn from usury limits.” Certainly, Adam Smith, of all individuals, favored usury limits so extra credit score would movement from “prodigals and projectors” towards extra “sober” debtors.

There’s empirical proof of credit score reallocation as properly. Hodenborn finds usury limits within the 19th century led banks to favor safer debtors “to the detriment of small, subprime debtors.” A examine of usury limits in Peru discovered that banks made fewer small loans and extra medium-sized ones, “favoring incumbent companies on the expense of latest debtors.” Our paper seems for proof of credit score reallocation within the context of a contemporary usury restrict within the U.S.

Our Examine

We examined how credit score modified in three states that enacted 36 % price caps someday between 2016 and 2022 (Illinois, South Dakota, and North Dakota). Our credit score knowledge are from the New York Fed Client Credit score Panel/Equifax (CCP). The CCP tracks quarterly credit score profiles for an anonymized random pattern of 5 % of households coated by the Equifax credit score bureau. The pattern includes over 35 million debtors. We measure borrower creditworthiness with the Equifax Threat Rating 3.0; scores vary between 350 and 800 and improve with creditworthiness.

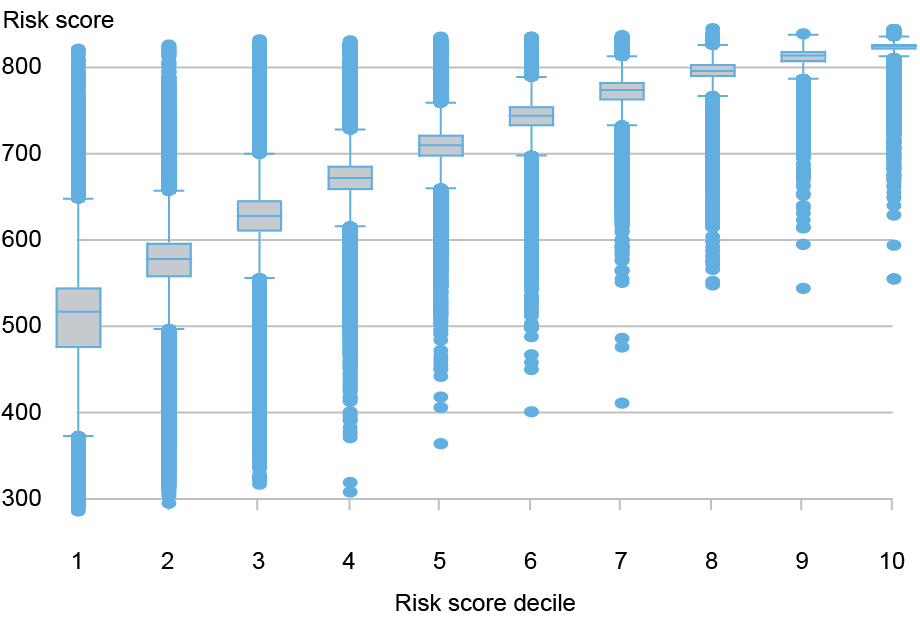

The chart beneath shows the distribution of danger scores for the three states that enacted a usury restrict between 2016 and 2022. Particularly, the chart exhibits the breakdown of debtors inside every danger rating decile, exhibiting the detailed distribution of danger scores inside every decile. The chance rating deciles are outlined based mostly on danger scores within the yr earlier than the usury restrict handed (see our Employees Report for particulars). The median danger rating within the lowest decile is about 518.

Threat Scores within the Lowest Decile Are About 150 Factors Beneath Prime on Common

Notes: This chart exhibits the distribution of danger scores by danger rating decile for households in Illinois, North Dakota, and South Dakota; households with the bottom scores are within the first decile. Threat scores are as of the yr earlier than usury limits took impact. The middle line in every field represents the median rating in that decile. The highest and backside of every field signify the twenty fifth and seventy fifth percentiles of danger scores, respectively, in that decile. The interquartile vary is the distinction between the seventy fifth and twenty fifth quartiles.

Within the absence of rate of interest caps, high-cost lenders concentrate on extending credit score to higher-risk (low danger rating) debtors which might be typically prevented by conventional, extra risk-averse lenders corresponding to banks and credit score unions. Within the presence of usury limits, these lenders could as a substitute select to lend extra to barely extra creditworthy debtors, for whom the usury restrict doesn’t bind. As an example, the median danger rating within the third decile is round 620, which is the normal cutoff for whether or not a borrower is subprime or prime. Lenders could prolong newly out there credit score to prime debtors after usury limits make lending to subprime debtors unprofitable.

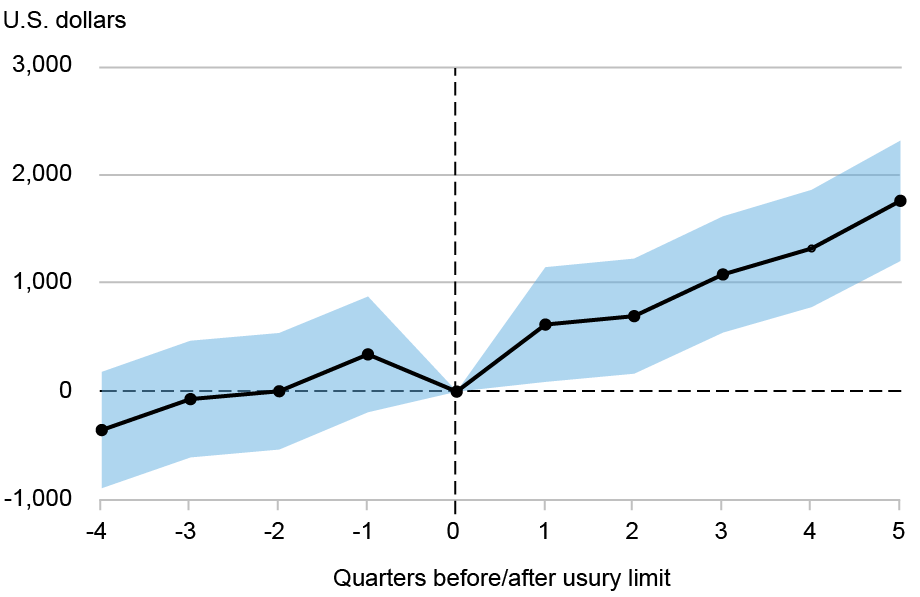

The chart beneath exhibits the rise in borrowing over time for the third danger rating decile relative to all larger deciles. Comparable will increase in borrowing are noticed within the fourth and fifth danger rating deciles relative to all larger deciles. The outcomes from these graphical analyses are per lenders reallocating credit score to comparatively extra creditworthy debtors after the imposition of usury limits. Additional per this view, within the Employees Report we present that whereas borrowing declines considerably for debtors within the lowest danger rating decile, solely a marginal decline is noticed within the combination. This means that the rise in lending to debtors within the third by fifth danger rating deciles principally offsets the decline in lending to debtors within the second danger rating decile.

Debtors within the Center of the Threat Rating Distribution See Elevated Lending after Fee Caps Relative to Management States

Be aware: This chart exhibits how debt balances modified for debtors within the third danger decile in Illinois, North Dakota, and South Dakota relative to their counterparts in management states.

Conclusion

Within the earlier publish, we discovered that lenders cut back credit score to the least creditworthy debtors after usury limits are imposed. On this publish, we present proof that lenders concurrently improve credit score to marginally extra creditworthy debtors. Whether or not this reallocation was an intention of the proposer of the bounds is unclear. In any case, our outcomes suggest that there could also be tradeoffs concerned in enacting usury limits, with some debtors going through extra hostile outcomes as others profit.

Rajashri Chakrabarti is an financial analysis advisor within the Federal Reserve Financial institution of New York’s Analysis and Statistics Group.

Gabriel Leonard is a analysis analyst within the Federal Reserve Financial institution of New York’s Analysis and Statistics Group.

On the time this publish was written, Donald P, Morgan was a monetary analysis advisor within the Federal Reserve Financial institution of New York’s Analysis and Statistics Group. He’s now retired.

Thu Pham is a analysis analyst within the Federal Reserve Financial institution of New York’s Analysis and Statistics Group.

Lee Seltzer is a monetary analysis economist within the Federal Reserve Financial institution of New York’s Analysis and Statistics Group.

The way to cite this publish:

Rajashri Chakrabarti, Gabriel Leonard, Donald P. Morgan, Thu Pham, and Lee Seltzer, “The Unintended Results of Curiosity Fee Caps: Credit score Reallocation to Safer Debtors,” Federal Reserve Financial institution of New York Liberty Avenue Economics, June 3, 2026, https://doi.org/10.59576/lse.20260603b

BibTeX: View |

Disclaimer

The views expressed on this publish are these of the creator(s) and don’t essentially replicate the place of the Federal Reserve Financial institution of New York or the Federal Reserve System. Any errors or omissions are the duty of the creator(s).