{kind=link}

Many retirees in India face a easy drawback: they could personal a home value ₹50 lakh, ₹1 crore, or much more, however nonetheless battle to pay their month-to-month payments after retirement. In different phrases, they’re asset wealthy however money poor.

A reverse mortgage is made for this precise scenario. It lets senior residents flip a part of their residence’s worth into common revenue with out promoting the home or shifting out. In easy phrases, the home retains working for you when you proceed dwelling in it.

Though Reverse Mortgages have been accessible in India for a number of years, only a few folks perceive how they work, and adoption stays extraordinarily low in comparison with Western nations. Allow us to perceive the idea in easy phrases.

What’s a Mortgage?

To grasp a reverse mortgage, begin with a standard mortgage. A mortgage is just while you pledge your property (like a home) as safety for a mortgage.

Instance:

Mr. A desires to purchase a home value ₹60 lakh. He places ₹10 lakh from his financial savings and takes ₹50 lakh from a financial institution. The financial institution retains the home as collateral till he repays the mortgage. That is known as a mortgage.

In a standard residence mortgage:

- The financial institution provides you cash.

- You repay by way of EMIs.

- The mortgage steadiness goes down over time and your fairness (possession share) in the home goes up.

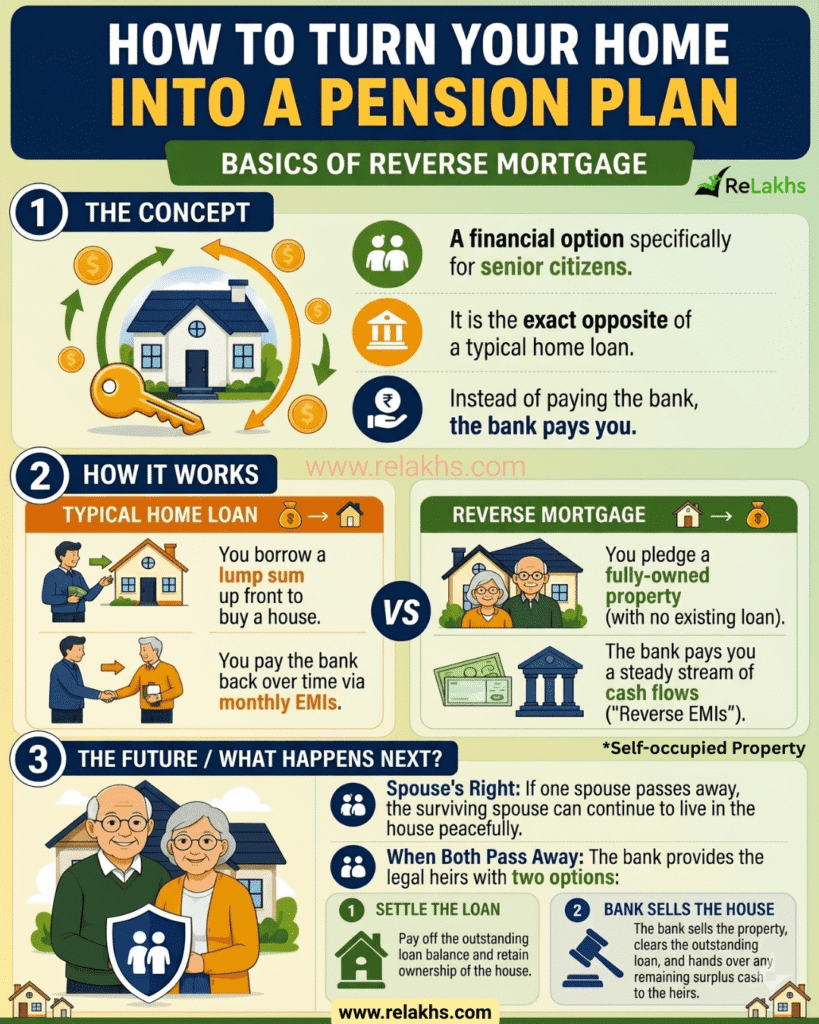

What’s a Reverse Mortgage?

A reverse mortgage works in the other way of a standard residence mortgage. As a substitute of you paying EMIs to the financial institution, the financial institution pays you.

On this association, a senior citizen pledges their self-occupied residence (residential) and receives common funds, a lump sum, or a mix of each. The house owner continues dwelling in the home for all times, and there may be normally no have to make month-to-month repayments through the mortgage tenure.

Reverse Mortgage | Easy Illustration

Assume:

- Age of house owner: 65 years

- Residential Self-occupied Property worth: ₹1 crore

- Home absolutely owned and free from present loans

The financial institution could supply a reverse mortgage, however normally not the total ₹1 crore. It considers solely a portion of the property worth primarily based on its inner valuation (Mortgage to Worth Ratio).

The financial institution could present:

- Month-to-month revenue

- Quarterly revenue

- Annual revenue

- Partial lump-sum for particular wants

The house owner continues dwelling in the home, and in contrast to a daily residence mortgage, no EMI is required.

Instance : Meet Mr. Ramesh, a retiree who owns a ₹1 crore flat in Mumbai however has a tiny pension and excessive medical payments. As a substitute of promoting his residence, he will get a reverse mortgage from a financial institution. The financial institution agrees to pay him ₹20,000 each month for the following 15 years, and Mr. Ramesh by no means has to pay a single month-to-month EMI. He and his spouse proceed dwelling of their residence peacefully with their bills absolutely lined.

Years later, after each go away, the overall mortgage steadiness (with accrued curiosity) stands at ₹85 lakh. The financial institution sells the flat at its present market worth of ₹1.5 crore, recovers the ₹85 lakh debt, and legally palms over the remaining ₹65 lakh in money straight to their daughter.

Conventional Residence Mortgage Vs Reverse Mortgage

| Particulars | Conventional Residence Mortgage | Reverse Mortgage |

|---|---|---|

| Function | To buy or assemble a home | To generate revenue from an already owned home |

| Who Receives Cash? | Borrower receives a lump-sum mortgage from the financial institution | Home-owner receives periodic funds from the financial institution |

| Month-to-month Funds | Borrower pays EMIs to the financial institution | Financial institution pays revenue to the house owner |

| Property as Safety | Home is mortgaged to the financial institution | Home is mortgaged to the financial institution |

| Excellent Mortgage Steadiness | Decreases over time as EMIs are paid | Will increase over time as funds and curiosity accumulate |

| Possession of Property | Stays with the borrower | Stays with the house owner throughout his/her lifetime |

| Proper to Keep within the Home | Borrower continues to dwell in the home | Home-owner continues to dwell in the home |

| Goal Viewers | People trying to purchase a house | Senior residents searching for extra retirement revenue |

| Reimbursement Throughout Lifetime | Necessary EMI funds | Typically, no EMI funds required |

| What Occurs After Loss of life? | Mortgage is normally repaid by authorized heirs or from insurance coverage proceeds | Heirs could repay the excellent mortgage and retain the property, or the property could also be offered by the financial institution to get better dues |

Eligibility Standards for Reverse Mortgage in India

Whereas particular phrases fluctuate barely by financial institution, the Reserve Financial institution of India (RBI) units down these normal standards:

- Age Requirement: The first house owner have to be 60 years or older. If making use of collectively with a partner, the partner should sometimes be a minimum of 55 years previous.

- Property Sort: The property have to be residential and self-occupied (you should really dwell there, not hire it out).

- Clear Title: The property have to be legally owned by you with a transparent, marketable title free from present loans or authorized disputes.

- Property Life: The home should have an affordable remaining lifespan (normally a minimal of 20–25 years) decided by a financial institution valuer.

What Occurs After the Borrower’s Lifetime?

This is among the most misunderstood components of a reverse mortgage. After the borrower (or the surviving partner, in a joint mortgage) passes away, the authorized heirs have two major choices:

Possibility 1: Repay the mortgage and preserve the property – The heirs can repay the excellent quantity together with accrued curiosity and retain possession of the home.

Possibility 2: Let the property be offered – If the heirs don’t wish to repay, the lender can promote the property. The financial institution recovers its dues, and the remaining steadiness goes to the authorized heirs. So, the financial institution doesn’t routinely turn into the proprietor. The authorized heirs proceed to have rights and selections.

Banks Providing Reverse Mortgage in India

A number of public sector banks and housing finance firms supply reverse mortgage merchandise, together with:

- State Financial institution of India (SBI)

- Punjab Nationwide Financial institution (PNB)

- Financial institution of Baroda

- Central Financial institution of India

- Union Financial institution of India

- IDBI Financial institution

- Axis Financial institution

- Varied Housing Finance Firms (like LIC Housing Finance)

Nonetheless, availability, eligibility norms, and product options can change over time. So, in case you are , test the most recent phrases immediately with the respective lender.

Taxation of Reverse Mortgage

Below Part 10(43) of the Revenue Tax Act, the periodic quantities acquired by a senior citizen below a reverse mortgage scheme are handled as a mortgage mortgage receipt, not revenue. Subsequently, they’re 100% exempt from revenue tax.

Additionally, merely mortgaging your property below a reverse mortgage does not set off capital positive aspects tax. Capital positive aspects could come into the image provided that the property is ultimately offered.

Why Is Reverse Mortgage Not In style in India?

Despite the fact that reverse mortgage has been accessible for a few years, it has not gained a lot traction in India. A number of key components clarify this.

1. Emotional attachment to property: For a lot of Indian households, a home is not only an asset. It’s seen as a legacy for kids and grandchildren. Many retirees hesitate to make use of their residence to generate retirement revenue.

2. Want to go away inheritance: Indian mother and father typically prioritize passing property to their youngsters. Lowering the worth accessible to heirs is normally seen negatively.

3. Ignorance: Many individuals merely have no idea that this product exists. Even financially educated people could not perceive how a reverse mortgage works.

4. Misconceptions: Frequent myths include-

- The financial institution will take the home instantly.

- The borrower loses possession rights.

- Kids completely lose inheritance rights.

These beliefs discourage folks from attempting it.

5. Decrease loan-to-value ratios: Banks don’t lend the total market worth of the property. Because of this, anticipated month-to-month payouts could also be decrease than what owners anticipate. Typically, the month-to-month payout will be capped.

6. Household and social components: In India, aged mother and father typically dwell with youngsters or anticipate household help. This reduces the demand for unbiased retirement revenue options like reverse mortgage.

Remaining Ideas

A reverse mortgage is a extremely sensible, safe monetary software—however it’s not a one-size-fits-all miracle. For some retirees, it could considerably enhance monetary independence and high quality of life after retirement. For others, the will to protect the property for future generations could also be extra essential than the revenue it offers.

The secret’s to know the idea clearly and test whether or not it matches your retirement objectives, household scenario, and monetary wants.

A house is not only a spot to dwell—it can be a helpful monetary asset when used correctly.

Proceed studying:

(Submit first printed on : 08-June-2026)