{kind=link}

Most mutual fund traders take a look at previous returns first. Questions like “Which fund gave the very best 5-year return?”, “Which fund has the very best CAGR?”, or “Which fund has a 5-star score?” come up on a regular basis.

And sure, returns matter. However they’re just one a part of the image.

Consider two fairness mutual funds that each delivered 15% annual returns over the past 5 years. Fund A achieved that with comparatively regular efficiency, whereas Fund B went by sharp ups and downs alongside the best way. Most traders would naturally choose Fund A, as a result of it gave the identical return with much less stress.

That’s the true level: in the case of investing, danger issues simply as a lot as return.

Why Ought to You Look Past Returns?

Greater returns typically include larger danger. An fairness mutual fund that tops the return charts throughout a bull market might also fall rather more sharply throughout a market correction. When you chase the highest-returning fund with out understanding the danger behind it, you would face disagreeable surprises when the market will get unstable.

That’s the place danger and risk-adjusted return measures change into helpful. These instruments allow you to perceive:

- How a lot danger the fund is taking

- Whether or not the fund supervisor is including actual worth

- How unstable the fund is in comparison with its friends

- How effectively it converts danger into returns

As an alternative of trying solely at returns, it’s higher to guage returns in relation to the dangers taken. That provides you a clearer image of what you’re actually investing in.

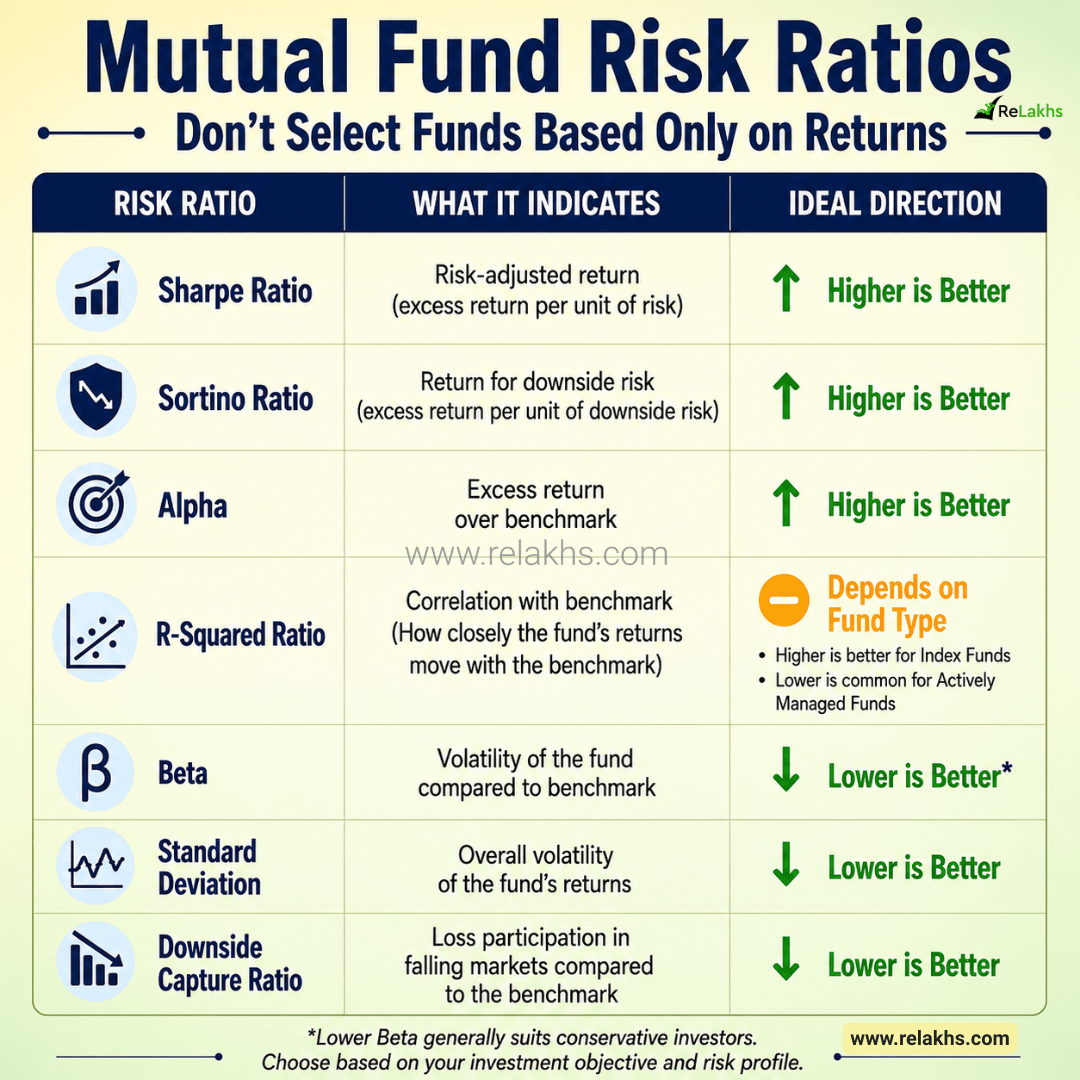

Key Threat & Threat-Adjusted Return Measures for Fairness Mutual Funds

1. Sharpe Ratio

What’s the Sharpe Ratio? The Sharpe Ratio tells you the way a lot further return a mutual fund offers you for each unit of complete danger it takes. In easy phrases, it solutions the query: “Did the fund reward traders sufficient for the danger it took?”

How one can interpret it

- Greater Sharpe Ratio = Higher risk-adjusted efficiency

- Decrease Sharpe Ratio = Much less environment friendly (the fund is taking extra danger for a similar return)

Instance: Suppose two funds each delivered 15% returns.

- Fund A: 15% return, Sharpe Ratio = 1.40

- Fund B: 15% return, Sharpe Ratio = 0.95

Though returns are the identical, Fund A is taken into account higher as a result of it generated these returns extra effectively, with much less danger per unit of return.

2. Sortino Ratio

The Sortino Ratio is much like the Sharpe Ratio, however with one key distinction. As an alternative of contemplating all volatility, it focuses solely on draw back volatility. Traders normally don’t fear when costs rise sharply. What actually issues is when investments fall. The Sortino Ratio is constructed to measure that dangerous volatility.

How one can interpret it

- Greater Sortino Ratio = Higher

- A better worth means the fund generated robust returns whereas holding draw back danger low

In easy phrases, the Sortino Ratio helps you see how effectively a fund protects your cash throughout market drops, not simply how a lot it grows when markets are upbeat.

3. Alpha

Alpha measures how effectively a fund supervisor can generate returns above the benchmark after adjusting for market actions. In easy phrases, it asks: “Did the fund supervisor truly add worth?”

How one can interpret it

- Constructive Alpha = Fund outperformed the benchmark

- Damaging Alpha = Fund underperformed the benchmark

Instance: If the benchmark returned 12% and the fund delivered 15%, the Alpha could possibly be +3% after adjusting for market danger. A constantly constructive Alpha normally exhibits good inventory choice and portfolio administration.

4. R-Squared (R²)

R-Squared measures how carefully a mutual fund’s returns transfer consistent with its benchmark index. In contrast to different ratios, R-Squared is neither inherently good nor dangerous; its that means is determined by the kind of fund.

For Index Funds – A excessive R-Squared (usually above 90) is fascinating as a result of the target is to carefully monitor the benchmark.

For Actively Managed Fairness Funds – A decrease R-Squared is completely regular. It merely exhibits that the fund supervisor is taking unbiased choices relatively than following the benchmark carefully.

For actively managed funds, Alpha and Beta typically matter greater than R-Squared alone.

5. Beta

Beta measures how delicate a mutual fund is to general market actions.

How one can interpret it

- Beta = 1 → Fund strikes broadly consistent with the market

- Beta > 1 → Fund is extra unstable than the market

- Beta < 1 → Fund is much less unstable than the market

Instance: If a fund has a Beta of 1.20, it might rise about 12% when the market positive aspects 10%. Equally, if the market falls 10%, the fund might drop round 12%.

Traders with decrease danger tolerance normally choose funds with a comparatively decrease Beta, as they are usually much less unstable throughout market swings.

6. Commonplace Deviation

Commonplace Deviation measures the general volatility of a mutual fund’s returns. A better normal deviation means the fund’s returns fluctuate extra. A decrease normal deviation signifies comparatively extra steady efficiency.

Instance: If two funds generate comparable long-term returns, the one with a decrease normal deviation will normally offer you a smoother funding journey.

7. Draw back Seize Ratio

This is among the most underrated but helpful measures. The Draw back Seize Ratio tells you the way a lot a mutual fund falls in comparison with its benchmark throughout declining markets.

How one can interpret it

- Decrease ratio = Higher draw back safety

Instance: Suppose the benchmark falls by 10%.

- Fund A falls by solely 7%

- Fund B falls by 12%

Fund A has higher draw back safety. Defending your capital when markets drop can considerably enhance long-term wealth creation.

What About Upside Seize Ratio? Whereas the Draw back Seize Ratio measures efficiency throughout falling markets, the Upside Seize Ratio measures how a lot of the benchmark’s positive aspects a fund captures throughout rising markets. Greater is mostly higher.

A robust fairness mutual fund ought to intention to:

- Seize a big portion of market positive aspects throughout bull markets (larger Upside Seize Ratio)

- Restrict losses throughout market corrections (decrease Draw back Seize Ratio)

In easy phrases, the perfect fund is one which rises extra when markets go up and falls much less when markets go down. Whereas no fund can constantly do that throughout all market cycles, these two ratios collectively give beneficial insights right into a fund’s danger administration and the way it performs in several market situations.

The place Can You Discover These Mutual Fund Threat Ratios?

Understanding the ratios is just step one. The following query is: “The place can I discover these danger measures earlier than investing?” There are a number of dependable locations the place these metrics are revealed.

1. Worth Analysis

One of the crucial extensively used mutual fund analysis web sites in India. You’ll find Sharpe Ratio, Sortino Ratio, Alpha, Beta, Commonplace Deviation, R-Squared, portfolio particulars, historic returns, and danger grades. It additionally permits you to examine a number of mutual funds throughout the similar class, making it simpler to shortlist appropriate schemes.

2. Morningstar India

Morningstar provides complete mutual fund analytics, together with risk-adjusted efficiency measures, Alpha, Beta, Commonplace Deviation, Sharpe Ratio, portfolio composition, and fund supervisor particulars. Its stories additionally embrace detailed commentary and magnificence evaluation.

3. Mutual Fund Factsheets

Each Asset Administration Firm publishes a month-to-month factsheet for every scheme. These normally embrace fund efficiency, portfolio holdings, Commonplace Deviation, Beta, Sharpe Ratio, portfolio turnover, sector allocation, and market-cap allocation. When you already personal a mutual fund, checking its month-to-month factsheet is an efficient behavior.

4. Different Mutual Fund Analysis Portals

A number of different monetary web sites and funding platforms additionally publish these danger measures and fund analytics.

Vital notice: The calculation interval (1 yr, 3 years, 5 years, and so on.) might fluctuate throughout platforms. So, each time attainable, examine funds utilizing knowledge from the identical supply.

Actual-Life Instance: Evaluating Two Small Cap Funds

Let’s examine two well-known small cap funds to grasp why traders ought to look past returns. Illustrative comparability solely. The figures under are indicative and should change over time. All the time discuss with the newest factsheets earlier than making funding choices.

Right here is the 5-year comparability knowledge for SBI Small Cap Fund and Nippon India Small Cap Fund based mostly on current common plan efficiency metrics:

| Metric | SBI Small Cap Fund | Nippon India Small Cap Fund | Higher Interpretation |

| 5-12 months Returns (CAGR) | ~14% | ~20% | Returns alone don’t inform the total story. |

| Sharpe Ratio | 0.41 to 0.45 | 0.68 to 0.76 | Greater is mostly higher (Threat-adjusted return). |

| Alpha | -3.97 to 4.06 | 0.54 to 1.36 | Greater is mostly higher (larger outperformance vs. benchmark) |

| Beta | 0.73 to 0.75 | 0.85 to 0.86 | Decrease might go well with conservative traders (decrease market sensitivity) |

| Commonplace Deviation | 14.59% to 17.11% | 14.54% to 19.55% | Decrease usually signifies decrease volatility (Smoother journey). |

| Draw back Seize | ~65% | ~68% | Decrease signifies higher draw back safety throughout market declines. |

Returns & Alpha: Nippon India Small Cap has traditionally delivered larger Alpha and absolute returns over the 5-year interval.

Volatility & Safety: SBI Small Cap, true to its status, maintains a decrease Beta and Commonplace Deviation, indicating a extra conservative stance relative to the broader small-cap swings. SBI constantly maintains a decrease Beta (0.73 – 0.75) in comparison with Nippon (0.85 – 0.86). That is the traditional trade-off: Nippon aggressively captures the upside, whereas SBI performs defensive.

A Few Sensible Suggestions

These ratios are helpful, however don’t choose a fund simply because it has the very best Sharpe Ratio or the bottom Beta. As an alternative, take a look at the whole image.

- Evaluate solely funds throughout the similar class.

- Favor funds with at the least a 5–10 yr monitor report.

- Overview a number of danger measures collectively, not only one ratio.

- Verify whether or not the fund supervisor stayed the identical throughout the analysis interval.

- Threat measures change over time, so assessment them periodically.

Bear in mind, these ratios are decision-support instruments—not decision-makers. They need to complement your evaluation of the fund’s funding goal, portfolio high quality, consistency of returns, expense ratio, and suitability on your monetary objectives.

Investing shouldn’t be about discovering the fund with the very best returns—it’s about discovering one which delivers constant, risk-adjusted efficiency. Earlier than investing in your subsequent fairness mutual fund, spend a couple of minutes reviewing these danger measures. They might help you make extra knowledgeable funding choices.

When you’ve got any questions, be happy to depart a remark under.

Proceed studying:.

(Publish first revealed on : 29-June-2026)

Disclaimer: This text is meant solely for academic functions. Mutual fund investments are topic to market dangers, and previous efficiency doesn’t assure future returns. Threat ratios, returns and different statistics mentioned on this article are dynamic and should change over time. The mutual fund examples are supplied solely to elucidate the ideas and shouldn’t be thought-about as purchase, promote or funding suggestions. All the time do your personal analysis or seek the advice of a certified monetary advisor earlier than making funding choices.