{kind=link}

Pidilite Industries Ltd – Constructing Bonds

Integrated in 1969 and headquartered in Mumbai, Pidilite Industries Restricted is India’s dominant adhesives and building chemical substances producer, with a model portfolio spanning client, institutional, and industrial segments. The corporate has constructed category-defining positions throughout adhesives, sealants, waterproofing, and floor care by means of manufacturers together with Fevicol, Fevikwik, M-Seal, Dr. Fixit, Roff, Araldite and WD-40. Its enterprise is organised into two verticals – Client and Bazaar (C&B), which incorporates retail-facing manufacturers bought by means of an intensive commerce community, and B2B, which addresses industrial, building venture, and pigment & preparations segments. Manufacturing is carried out throughout roughly 70 vegetation pan-India, supported by 50+ distribution centres and a vendor community spanning over 3.8 lakh retailers.

Merchandise and Providers

- Adhesives – Artificial resin, on the spot, epoxy and sealant adhesives underneath Fevicol, Fevikwik, M-Seal and Araldite for woodworking, client restore and industrial use.

- Waterproofing and Development Chemical substances – Full-spectrum waterproofing underneath Dr. Fixit and tile and stone fixing options underneath Roff, masking each retail and venture segments.

- Wooden and Floor Finishes – Wooden coatings by means of the ICA Pidilite JV and hotmelt adhesives.

- Ornamental Coatings and Sealants – Inside emulsion paints underneath Haisha, ornamental renders underneath UnoFin, and building sealants underneath Feviseal.

- Pigments and Preparations – VAM-based pigment emulsions and chemical preparations equipped to industrial and export prospects.

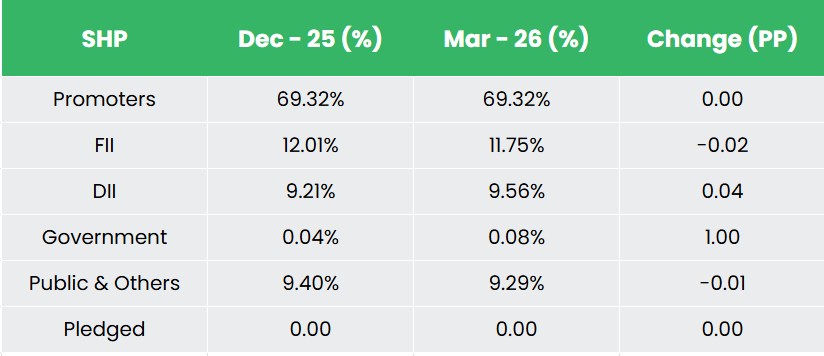

Subsidiaries: As of FY26, the corporate has 34 subsidiary firms, 7 Affiliate Firms and 1 Joint Enterprise.

Funding Rationale

- Quantity development inflection and working leverage – Pidilite’s standout characteristic in FY26 has been a transparent step-up in underlying quantity development (UVG) after eleven quarters within the 8-10% vary. Full-year UVG improved to ~11.1% from 9.3% in FY25, with Q4FY26 accelerating to fifteen.3%, led by each Client & Bazaar (15.4%) and B2B (14.8%). The acceleration was broad-based moderately than slender: the core Fevicol franchise delivered double-digit development alongside faster-growing manufacturers akin to Roff and Dr. Fixit on the higher finish of their bands. With the price base beneath gross margin largely mounted, every incremental level of quantity compounds working leverage – evident within the 310bps consolidated EBITDA margin enlargement in Q4FY26, solely ~100bps of which got here from gross margin. Administration has guided to systematically elevating UVG by ~100bps yearly whereas reinvesting margin headroom into demand technology, supporting a virtuous growth-leverage cycle.

- Laddered Core Progress portfolio with a protracted structural runway – Pidilite runs a intentionally laddered portfolio engineered to compound development throughout horizons. Its Core manufacturers – Fevicol, Fevikwik, M-Seal and Araldite, are category-defining franchises with dominant share and pricing energy, focused to develop at 1-2x GDP through premiumization and innovation. The Progress layer – Dr. Fixit, Roff, WD-40, Fevicryl and ICA wooden finishes addresses structurally under-penetrated classes rising at 2-4x GDP; The Pioneer layer seeds nascent classes together with ornamental paints (Haisha), waterproof renders (UnoFin), industrial joinery adhesives (Jowat) and electronics/EV adhesives. Anchored to India’s building, restore and home-improvement cycle, this structure offers a protracted, largely self-funded runway, with every layer maturing into the subsequent and frequently refreshing the corporate’s development profile.

- Model-led pricing energy and a robust distribution moat – Pidilite’s model fairness and distribution attain underpin its potential to soak up input-cost volatility. Towards a 40-50% rise in its weighted-average raw-material basket – pushed by VAM costs surging ~70% amid the West Asia battle, the corporate has taken calibrated value will increase of ~4-5% in April and an additional ~7-8% in Could at a blended degree (12-15% on the Fevicol portfolio), whereas prioritising quantity momentum over near-term margin seize. The moat rests on category-defining manufacturers that command pricing energy, paired with an unmatched route-to-market spanning ~3.8 lakh sellers, 40,000+ cities and 24,000+ branded Pidilite ki Duniya retailers, supported by wholesome VAM stock cowl. Administration has traditionally reinvested margin upside into deepening this attain moderately than maximising short-term profitability, steadily widening the hole versus the unorganised phase, which tends to battle by means of durations of supply-chain and pricing volatility.

- Q4FY26 – Throughout the quarter, the corporate reported a consolidated income of ₹3,583 crore, up 14.1% YoY from ₹3,141 crore in Q4FY25, underpinned by a pointy acceleration in underlying quantity development to fifteen.3%. EBITDA rose to ₹833 crore, a 31.7% enhance, with EBITDA margin increasing 310bps to 23.2%, pushed by ~100bps of gross-margin positive aspects and working leverage. Consolidated web revenue grew 36.6% YoY to ₹584 crore.

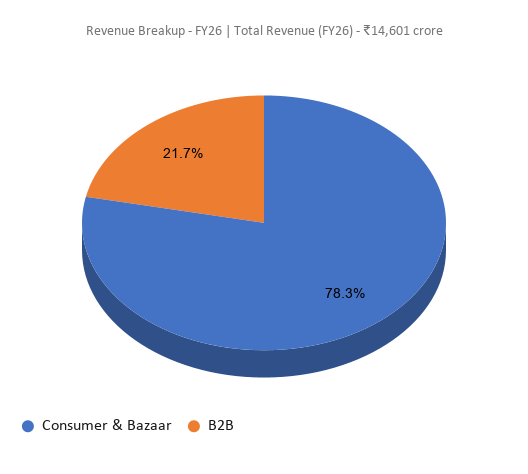

- FY26 – For FY26, consolidated income stood at ₹14,601 crore, up 11.1% YoY, with full-year UVG bettering to ~11.1% from 9.3% in FY25. EBITDA grew ~16.8% to ₹3,519 crore, with margin increasing 120bps to 24.1%. Consolidated web revenue rose 17.9% YoY to ₹2,471 crore.

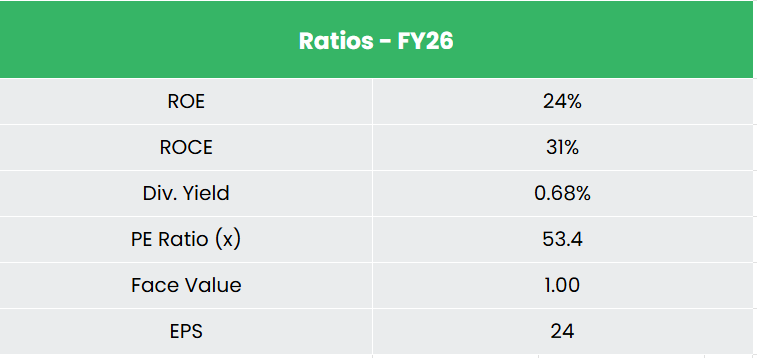

- Monetary Efficiency – The three-year income and web revenue CAGR stands at 7% and 25% respectively between FY24-26. The corporate has a debt-to-equity ratio of 0.04. The three-year common ROE and ROCE are round 23% and 30% for FY23-25 interval.

Business Overview

The Indian chemical sector is anticipated to succeed in US$ 1 trillion by 2040. India is the sixth largest producer of chemical substances on the planet and third in Asia, contributing 7% to India’s GDP. Inside this, the construction-chemicals and adhesives segments, are rising effectively forward of the broader economic system, supported by rising urbanisation, infrastructure spend and a structural shift from cement-based to chemical-based constructing options. The Indian specialty chemical substances sector is forecasted to develop at a CAGR of three.80% from 2025-33, reaching US$ 92.6 billion by 2033, pushed by sturdy demand from building, automotive and home-care finish makes use of alongside rising industrialisation and product innovation. World supply-chain de-risking away from China, premiumisation and a fast-expanding center class additional underpin a multi-year demand runway.

Progress Drivers

- 100% FDI permitted underneath the automated route within the chemical sector (besides a couple of hazardous chemical substances), inviting greenfield and brownfield funding.

- Rising middle-class households, projected to succeed in ~148 million by FY30 (7.4% CAGR), driving greater per-capita consumption of paints, adhesives and building chemical substances.

- Authorities infrastructure and housing push, together with the Nationwide Infrastructure Pipeline and PCPIR funding areas focusing on ~Rs. 20 lakh crore (US$ 276 billion) by 2035, accelerating construction-led chemical demand.

Peer Evaluation

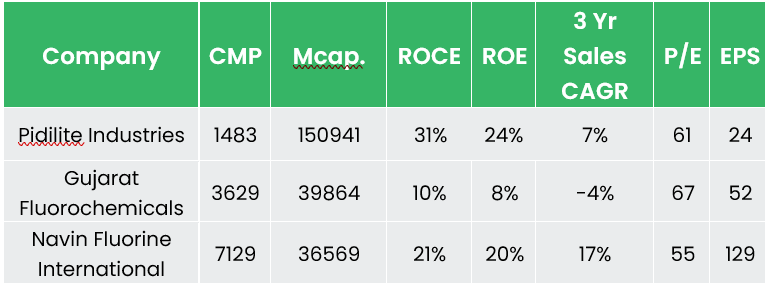

Rivals: Gujarat Fluorochemicals Ltd, Navin Fluorine Worldwide Ltd and so on.

The corporate boasts an business main return profile, and demonstrates disciplined capital allocation and superior margins, whereas sustaining an unencumbered stability sheet.

Outlook

Pidilite enters FY27 navigating a pointy uncooked materials value cycle whereas staying dedicated to its volume-first working philosophy. Administration has guided to sustaining the ~100 bps annual UVG step-up in keeping with FY26’s supply of ~11.1% versus 9.3% in FY25 – with double-digit UVG as the express inner goal and any margin headroom to be reinvested into demand technology moderately than captured. Administration has reaffirmed the 20–24% EBITDA margin hall as its standing steerage, acknowledging that FY27 will possible ship towards the decrease finish of that band given the inflationary atmosphere. Capex is guided to stay inside the 3–5% of income band, with FY26 spend already stepping as much as ~₹570 crore from ₹430 crore, and a big Fevicol and premium white glue plant in West India is on observe for commissioning in Q1FY27.

Valuation

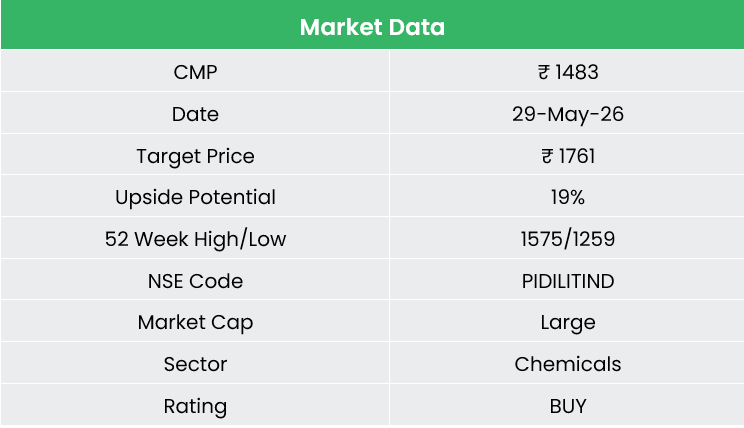

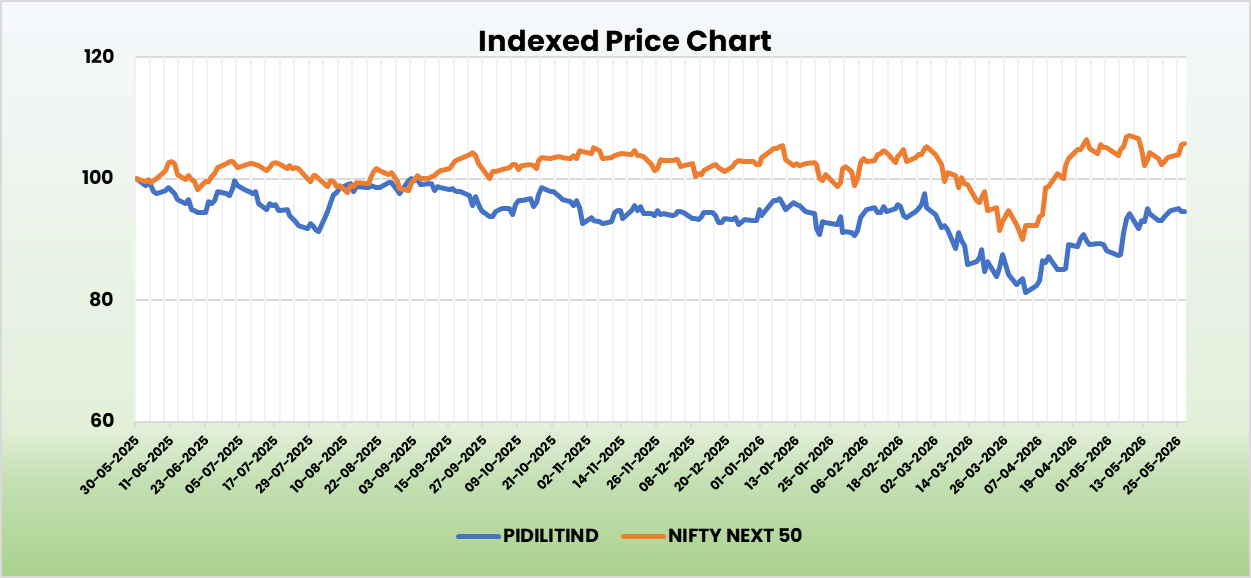

Pidilite’s category-defining model portfolio, the FY26 volume-growth inflection, and a distribution moat that widens by means of each value cycle place it as a structural compounder within the Indian client house. The present raw-material disruption, whereas pressuring near-term margins towards the decrease finish of the 20-24% hall, is prone to additional consolidate market share towards the organised chief. We advocate a BUY ranking on the inventory with a goal value (TP) of Rs. 1,761, 59x FY28E EPS, an upside potential of ~19%. We additionally encourage sustaining a stop-loss at 20% from the entry value to handle potential draw back threat successfully.

SWOT Evaluation

| Energy | Weak point |

|

|

| Alternatives | Threats |

|

|

Disclaimer: Investments within the securities market are topic to market dangers, learn all associated paperwork rigorously earlier than investing. Securities quoted listed below are exemplary, not recommendatory. Please seek the advice of your monetary advisor earlier than investing. Please be aware that we don’t assure any assured returns for the securities quoted right here.

Analysis disclaimer: Funding within the securities market is topic to market dangers. Learn all of the associated paperwork rigorously earlier than investing. Registration granted by SEBI, and certification from NISM by no means assure the efficiency of the middleman or present any assurance of returns to traders.

For extra particulars, please learn the disclaimer.

Different articles chances are you’ll like

Submit Views:

189