{kind=link}

I’ve stated this many occasions – financial coverage shouldn’t be match for objective and central banks must be prevented from having discretionary powers to change charges at will. There are two ranges of justification for that assertion. First, on the ideological stage, a serious (dominant below neoliberalism) arm of macroeconomic coverage shouldn’t be outsourced to an unelected, unaccountable physique of technocrats. This subverts the operation of democracies by permitting elected officers to depoliticise coverage settings by way of their ‘cross the parcel’ method – ‘oh the central financial institution is impartial and we by no means intervene of their choices’ sort narrative. Second, on a technical stage, the officers have little thought of when and what the influence can be of their coverage modifications. There are too many unknowns, principally referring to the distributional penalties of rate of interest modifications (collectors win, debtors lose) which make it unattainable to foretell when the collectors will spend up their positive aspects and debtors reduce their spending. In consequence, there are a lot of examples in historical past of central banks transferring too early (relative to their acknowledged goal) or too late, with the end result being that they make issues worse, notably prolonging recessions. This case is as soon as once more looming up in Japan for the time being.

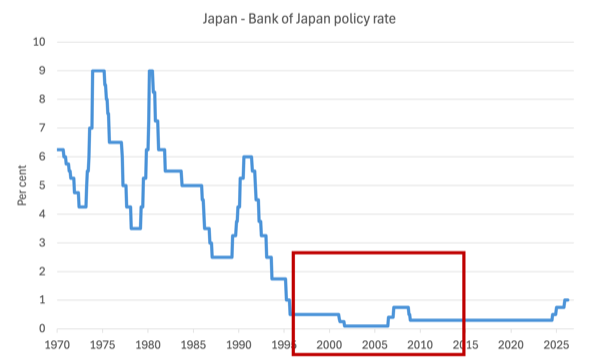

Right here is the Financial institution of Japan coverage price going again to the start of 1970.

However I wish to zero in on the interval main up the GFC (the rectangle space within the earlier graph) when Japan was going through rising crude oil costs had been extremely risky in historic phrases.

The see-sawing costs went from a mean $US56 per barrel in 2005, to $US66 pb in 2006 as Center East unrest triggered provide disruptions.

In 2007, the value moved above $US100 on the again of a surge in demand from the NICs and reached $US147.27 in July 2008.

The GFC emerged later within the 12 months and oil fell again to lower than $US40 pb in December.

In 2009, oil costs averaged $US61 pb on the again of the gradual financial restoration and pushed as much as $US80 by the tip of 2010.

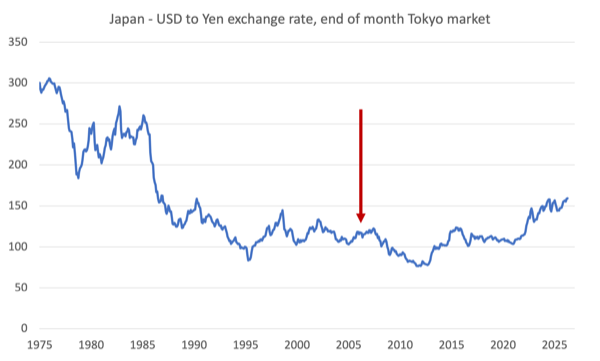

Throughout this era, the yen additionally depreciated towards the USD, see the subsequent graph.

By June 2007, it had reached a price of $US122.6986, a depreciation from its earlier low recorded in January 2005 of 15.8 per cent.

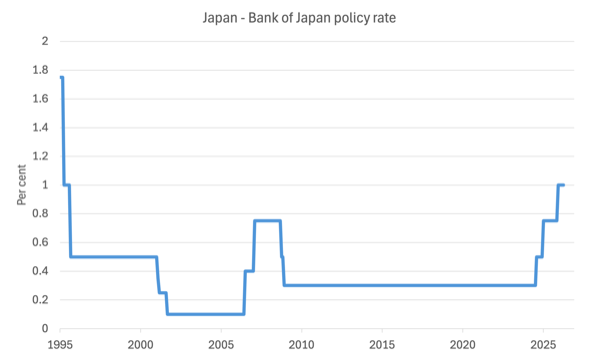

This graph reveals the Financial institution of Japan coverage price interval since 1995, to spotlight the response of the Financial institution to the oil worth volatility and the yen depreciation after 2005.

In January 2005, the coverage price was 0.1 per cent and had remained at that stage because the final reduce in September 2001, in response to nearly zero GDP development and an amazing deflationary gloom.

Inflation was round zero and at occasions detrimental.

On the time, the Financial institution of Japan was below the governorship of – Toshihiko Fukui – a profession central banker, who had beforehand been compelled to resign as Deputy Governor of the BoJ in 1998 over a bribery scandal when beneficial monetary info was leaked to the enterprise group.

Nevertheless after bowing loads, and getting the assist of his mates within the enterprise group, Fukui-san was put in as Governor by Prime Minister Junichirō Koizumi in 2003, and remained in that function till March 19, 2008.

The Financial institution of Japan fashioned the view below his governorship that although inflation was no subject, the Financial institution needed to tighten rates of interest simply in case, claiming that the depreciating yen would result in accelerating inflation.

They subsequently pushed charges up from 0.1 per cent to 0.75 per cent by February 2007.

GDP development slowed and was zero within the June-quarter 2007, then detrimental within the September-quarter 2007.

Through the interval 2005 to the tip of 2010, the annual CPI inflation price averaged -0.08 per cent, whereas vitality inflation was 1.7 per cent on common.

Through the interval January 2005 to December 2007, the annual common CPI inflation price was 0.15 per cent, and common vitality inflation was 3.74 per cent.

The depreciating yen didn’t result in an acceleration within the home inflation price however helped Japanese producers who had been struggling.

The Financial institution of Japan, pushed by a New Keynesian ideology, overreacted to the transitory price shocks arising from the vitality worth volatility and clearly didn’t have an excellent understanding of what was driving the deflationary pressures within the nation.

Somebody within the Financial institution acquired their US graduate economics textbooks out and concluded – vitality costs up, alternate price down, hyperinflation possible, resolution hike charges.

The yen worth was at its lowest in June 2007 and by the point Shirakawa took over as governor of the Financial institution in March 2008, it had appreciated towards the USD by some 17.9 per cent.

However Shirakawa held the New Keynesian line refusing to decrease rates of interest, which was curious on the time, given a serious cause that the Financial institution had hike within the first place in 2006 was tied to the fears that the depreciating yen would trigger an acceleration in CPI inflation.

CPI inflation quickly rose in early to mid-2008, predictably, as vitality costs surged, which was nothing to do with the Financial institution’s coverage settings a method or one other.

Then Lehman’s crashed and the yen continued to understand whereas the Financial institution reluctantly however too slowly reduce charges finally sustaining the low cost price at 0.3 per cent from December 2008 by way of to July 2024.

In the meantime, CPI inflation was detrimental from February 2009 by way of to Might 2013.

Japan was in a worsening recession from June 2008 to March 2009 (dropping 2.5 per cent each year within the December-quarter 2008 and 4.8 per cent within the March-quarter 2009).

From the time Shirakawa took workplace (March 2008) to the March-quarter 2009, the Japanese economic system contracted by 8.9 per cent, a large dent in materials prosperity, which bolstered the deflationary mindset that has plagued the Japanese individuals because the early Nineteen Nineties when the massive asset bubble burst.

Additional, whereas different central banks reduce charges extra aggressively after the Lehman crash, the tardy Japanese response saved the upward stress on the yen, which undermined the profitability of the Japanese producers, a few of which have by no means absolutely recovered.

The Financial institution of Japan thus missed the turning factors within the cycle at each ends as a result of they misunderstood the state of affairs on the time, which was largely being pushed by the vitality worth fluctuations that had been principally politically pushed (together with the Second Itifada, the loss of life of Yasser Arafat, and the ethnic and non secular unrest in Iran, Egypt and elsewhere).

And in doing in order that they made issues worse.

They need to by no means have hiked charges within the 2006 and having made that mistake they need to have reduce them a lot earlier and far sooner than they did.

They weren’t the one central financial institution that fully missed what was happening.

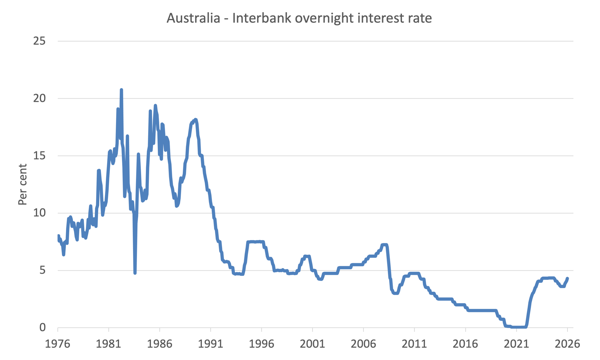

Right here is the RBA Money Price Goal from Might 1976 to Might 2026.

Within the lead as much as the main recession in 1991, the RBA pushed charges as much as over 18 per cent regardless of it changing into apparent {that a} important recession was looming.

Even when the nation skilled its worst downturn because the Nice Melancholy within the Nineteen Thirties and inflation had all however vanished, the RBA saved rates of interest at elevated ranges making the restoration a lot tougher than it ought to have been and sustaining mass unemployment at a lot greater ranges for longer than might have been the case.

The hardships for the working class throughout this era had been immense.

Then throughout the oil worth volatility in 2005 and on, the coverage makers once more grew to become obsessive about inflationary fears.

The RBA went into motion a lot earlier nevertheless, pushing charges up from early 2001.

Because the inflation paranoia elevated, the RBA went on steroids and elevated the speed 19 occasions between March 2005 and September 2008.

The speed went from 5.49 per cent in March 2005 to a excessive of seven.25 per cent by the point Lehman’s crashed.

It was apparent that inflation was benign and the vitality shocks had been transitory.

It was additionally apparent that unemployment was being held at elevated ranges for no cause.

Then the GFC shock got here and the RBA as soon as once more was too gradual to react within the different route.

It took a large fiscal intervention to maintain the economic system from fully collapsing in that interval whereas the RBA was reluctant to drop charges rapidly sufficient.

Then simply because the economic system was beginning to regain some momentum once more in late 2010, the RBA determined it wished to set the speed at some unobserved and ideologically-contrived impartial price, which led it to begin mountain climbing once more in November 2010.

The restoration stalled (the financial coverage influence was exacerbated by the fiscal contraction on the similar time).

It was ridiculous.

And now we’re again there once more

The Financial institution of Japan (and the RBA and different central banks) are as soon as once more mountain climbing charges or planning to hike additional within the face of the vitality worth rises arising from the stupidity of Trump and Bibi.

In Japan, the yen has once more depreciated – by 34 per cent since March 2022.

CPI inflation stays reasonable however the BoJ has hiked from 0.3 per cent in March 2022 to 1 per cent now.

The depreciation is essentially on account of differential development charges in Japan and the US and the truth that Japan initially didn’t reply to the COVID-induced inflationary pressures as rapidly because the US Federal Reserve.

That differential response noticed speculative funding capital move out of the yen into the USD.

It barely triggered a dent within the CPI inflation price however was a lift to Japanese producers.

It is usually clear that the Japanese authorities desires to pursue an (reasonably) aggressive fiscal enlargement to be able to break the nation out of its deflationary mindset that has led to:

1. Firms sitting on giant stockpiles of retained earnings and refusing to put money into new capital.

2. Firms refusing to supply sturdy wages development.

3. Firms refusing to greater common, full-time employees and choosing up the fluctuations in demand by way of using non-regular (informal and part-time) employees.

4. Shoppers, going through much less safe work and flat nominal wages (and declining actual wages) refusing to cut back their saving ratio and spend extra on consumption.

That mindset is entrenched and can take a serious shock to interrupt out of it.

Ms. Takaichi appears to know that and realises that a big fiscal shock is required (through public infrastructure funding) to supply confidence to the non-public sector that the nation is popping in the direction of optimism.

Whereas there are some early indicators of that taking place, the firms are nonetheless sitting on the massive stockpiles of financial savings and the non-public funding ratio stays caught.

The newest CPI information reveals the inflation is dropping rapidly in Japan.

The much-watched Tokyo inflation gauge fell to its slowest tempo in 4 years – CPI excluding recent meals got here it at 1.3 per cent for the 12 months to Might 2026.

There have additionally been six consecutive declines within the price.

The general All teams CPI recorded an annual inflation price of 1.4 per cent.

In the meantime, lively fiscal coverage – subsidies for utility (water) prices, childcare have additionally helped households.

The commentary is all too acquainted although.

I learn every single day statements like “There is no such thing as a sturdy momentum in inflation however upside dangers are looming giant as a result of Iran battle” (Supply).

Upside dangers!

Central financial institution converse.

However in the event you put all the knowledge collectively – excessive retained earnings persist, giant depreciation, low inflation and many others – the mainstream narrative that rates of interest should rise is unjustifiable.

Regardless of that the BoJ is below stress to proceed its present price mountain climbing cycle – which might be disastrous.

First, the banking sector is incomes important returns on the reserve balances it has with the BoJ courtesy of the years of quantitative easing the place the BoJ alternate reserves for presidency bonds.

Each time the BoJ hikes charges additional, the revenue flowing from the assist funds on these reserve balances rise.

The shareholders do nicely however the economic system declines.

Second, the depreciation is being ‘managed’ by the Division of Finance interventions into the foreign exchange market and the decrease worth helps Japanese exporters, whereas the Authorities is offering fiscal assist to ease the burden of upper import costs on households.

Third, the BoJ is already creating large disruption within the Japanese authorities bond markets by way of its so-called Quantitative Tightening (QT) program, the place it sells off its giant stockpile of JGBs again into the secondary bond market.

The consequence has been to drive down bond costs and push yields up – as the provision of JGBs into the market will increase due to QT.

The rising yields are seen by the Authorities as an issue and is thus inserting immense stress on the BoJ to not push charges any greater.

The federal government stress to decrease charges is working towards the stress from bankers and economists for the BoJ to push charges greater.

It’s a mess.

However the BoJ officers ought to evaluation their very own historical past (of which I’ve offered a glimpse) and realise they often act in a misguided method and make the state of affairs worse.

Conclusion

At current there is no such thing as a endemic long-term, entrenched inflation downside.

Ultimately the folly within the Center East can be over in a method or one other and oil costs will drop once more.

Central banks ought to simply ‘look by way of’ (jargon) the non permanent disruptions and depart charges on maintain (or reduce them).

Then lock the door and inform the Treasury departments to take over.

That’s sufficient for as we speak!

(c) Copyright 2026 William Mitchell. All Rights Reserved.