{kind=link}

Retirement planning in India is commonly misunderstood. Many individuals assume any long-term financial savings or funding plan can provide them a pension, however that’s not true. Only some choices are literally designed to present you a daily earnings after retirement.

That distinction issues as a result of retirement isn’t just about constructing a corpus. It’s about ensuring cash retains coming in even after your energetic earnings stops.

In India, true pension choices are restricted. There are numerous financial savings and funding merchandise, however solely a handful actually qualify as pure pension schemes—those who flip your contributions right into a month-to-month earnings throughout retirement. A few of these are obligatory relying in your job, whereas others are voluntary and wish you to choose in.

On this article, let’s break down the 5 important pension schemes in India—

- Staff’ Pension Scheme (EPS)

- Nationwide Pension System (NPS)

- Atal Pension Yojana (APY)

- Insurance coverage-based pension plans and

- Superannuation schemes.

We’ll preserve it easy and canopy their options, eligibility, lock-in guidelines, and execs and cons so you possibly can see which of them truly suit your retirement plan.

Pension Oriented Schemes in India – Full Information

Planning for retirement is not nearly “saving”; it’s about choosing the proper car to fight inflation and guarantee a gentle earnings. Here’s a breakdown of the highest 5 pension-related schemes in India

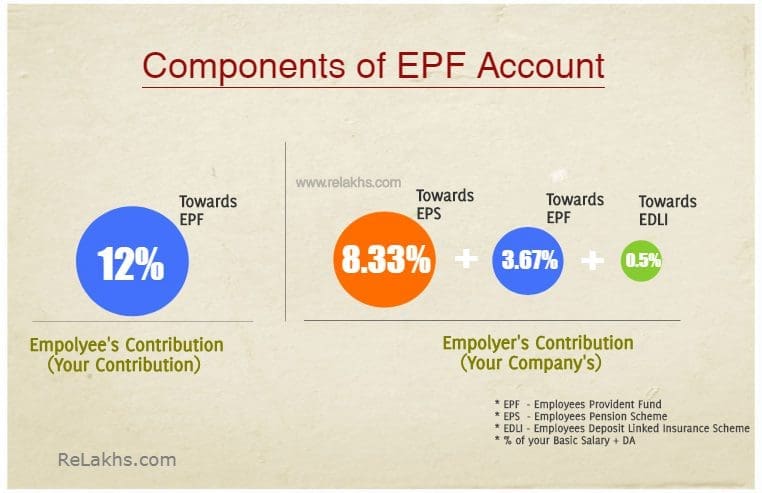

1) Staff’ Pension Scheme (EPS)

Managed by the EPFO, it is a social safety scheme for organized sector workers.

- Who can subscribe: Any worker who’s a member of EPF.

- Key function: 8.33% of the employer’s contribution goes into this pension fund.

- Eligibility: At the very least 10 years of service and age 58.

- Lock-in / Exit: Locked until retirement, although early pension can begin from age 50 with a decreased payout.

- 2026 replace on withdrawal: The pension half can now be withdrawn solely after 36 months of leaving the job, as a substitute of two months.

- Additionally, not less than 25% of your PF stability should keep untouched till retirement so you retain a fundamental pension base.

Execs: Assured lifelong pension, plus survivor advantages for partner and kids.

Cons: Returns are mounted and formula-based, so often decrease than market-linked schemes. It’s obligatory for workers incomes as much as ₹15,000 fundamental wage.

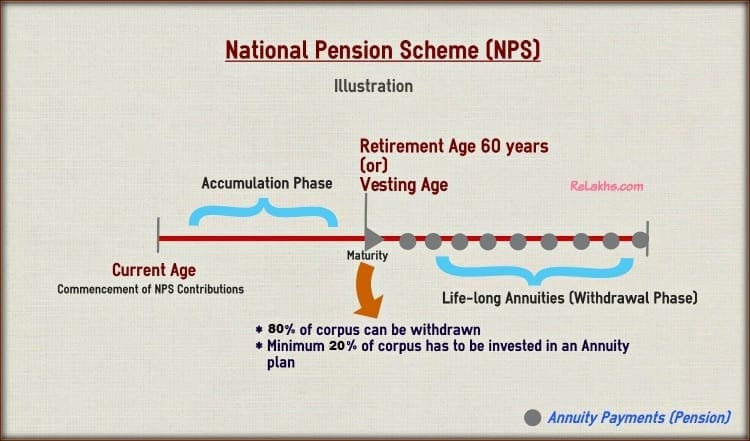

2. Nationwide Pension System (NPS)

A market-linked, voluntary retirement scheme regulated by the PFRDA. It’s extensively thought of essentially the most versatile pension software in 2026.

- Who can subscribe: All Indian residents (together with NRIs and OCIs) aged 18–85.

- Key Options: Alternative of funding (Fairness, Company Bonds, Authorities Bonds). Consists of NPS Vatsalya for minors.

- 2026 Replace – Withdrawal Guidelines:

- Maturity (Age 60): Now you can withdraw as much as 80% as a tax-free lump sum (elevated from 60%). The remaining 20% should be used for an annuity.

- Full Exit: If the full corpus is ≤ ₹8 Lakh, you possibly can withdraw 100% with out shopping for an annuity.

- Untimely: Partial withdrawals (as much as 25% of personal contributions) allowed for particular causes (training, sickness) after 3 years.

Execs: Excessive return potential; additional tax deduction of ₹50,000 (Sec 80CCD(1B)); lowest administration charges globally.

Cons: Market-linked (returns aren’t assured); annuity earnings is taxable.

Vital Observe: In contrast to conventional pension schemes, NPS itself doesn’t assure a pension. It builds a retirement corpus, and you will need to convert a portion of it into an annuity to generate month-to-month earnings. It’s essential to purchase an annuity plan from a life insurer. The standard of your pension beneath NPS relies upon not simply in your corpus, but additionally on the annuity charges obtainable at retirement.

Replace: Unified Pension Scheme (UPS)

The federal government has launched the Unified Pension Scheme (UPS) for central authorities workers in its place framework alongside NPS. In contrast to NPS, which is market-linked, UPS goals to offer a extra predictable pension construction (Assured pension + contribution-based construction). Nonetheless, this scheme is at present restricted to authorities workers and isn’t obtainable for most of the people.

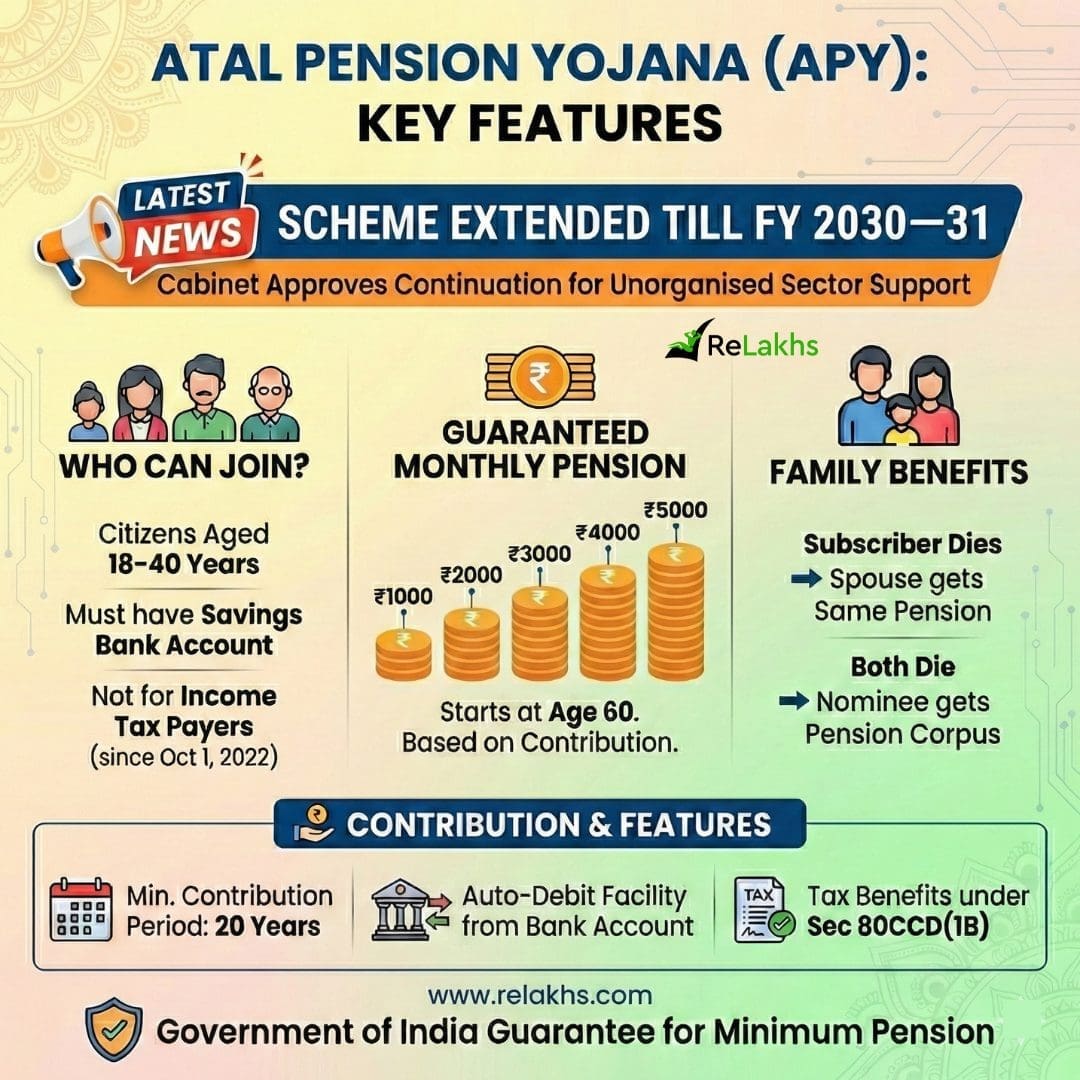

3. Atal Pension Yojana (APY)

Authorities-backed scheme primarily for unorganized sector staff, guaranteeing a minimal pension.

- Who can be a part of: Indian residents aged 18–40.

- Observe: Earnings tax payers can’t be a part of since 2022.

- Key options: Mounted pension choices—₹1,000, ₹2,000, ₹3,000, ₹4,000, or ₹5,000 month-to-month.

- Withdrawal guidelines:

- Maturity: Auto-starts at age 60

- Untimely: Not allowed (besides terminal sickness or dying)

Execs: Govt assure + triple profit (you → partner → corpus to nominee). Appropriate for low-income people

Cons: Entry capped at 40 years; mounted pension gained’t beat excessive inflation.

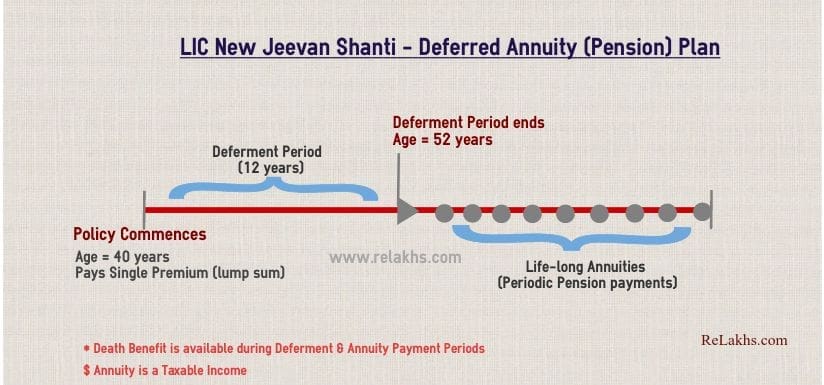

4. Life Insurance coverage Pension Schemes

Non-public/Public insurance coverage firms (like LIC, SBI Life) supply “Annuity” or “Retirement” plans.

- Who can subscribe: Anybody (usually entry age 18–70).

- Eligibility: Based mostly on the particular coverage’s well being and age standards.

- Key Options: Two phases—Accumulation (paying premiums) and Vesting (receiving pension/annuities).

- Forms of Annuities:

- Deferred annuity: Construct corpus first (accumulation section), then convert to pension later.

- Instant annuity: Pension begins straight away after one-time funding.

- Withdrawal Guidelines:

- Lock-in: Usually 3–5 years.

- Maturity: Often, 60% will be taken as a lump sum (tax-free guidelines apply per Part 10(10D)), and 40% is annuitized.

Execs: Mounted, assured earnings choices (conventional plans); dying profit (life cowl) usually bundled.

Cons: Excessive give up fees if exited early; decrease returns in comparison with NPS.

5. Superannuation (Tremendous Annuity)

Employer-sponsored pension scheme managed by way of authorised superannuation funds. It’s a company pension program the place the employer contributes to a fund for the worker’s retirement.

- Who can be a part of: Staff of firms providing superannuation advantages.

- Key options: Employer contributes as much as 15% of fundamental wage (outlined contribution or profit).

- Withdrawal guidelines:

- Retirement: Withdraw 1/third (33.3%) tax-free lump sum. Remaining 2/third → should purchase annuity. (Much like NPS construction)

- Job change: Switch to new employer’s fund or preserve till retirement or Withdraw (tax implications).

Execs: Massive corpus from employer cash + tax-free contribution as much as ₹1.5 lakh.

Cons: Just for company workers; inflexible 1/third withdrawal rule.

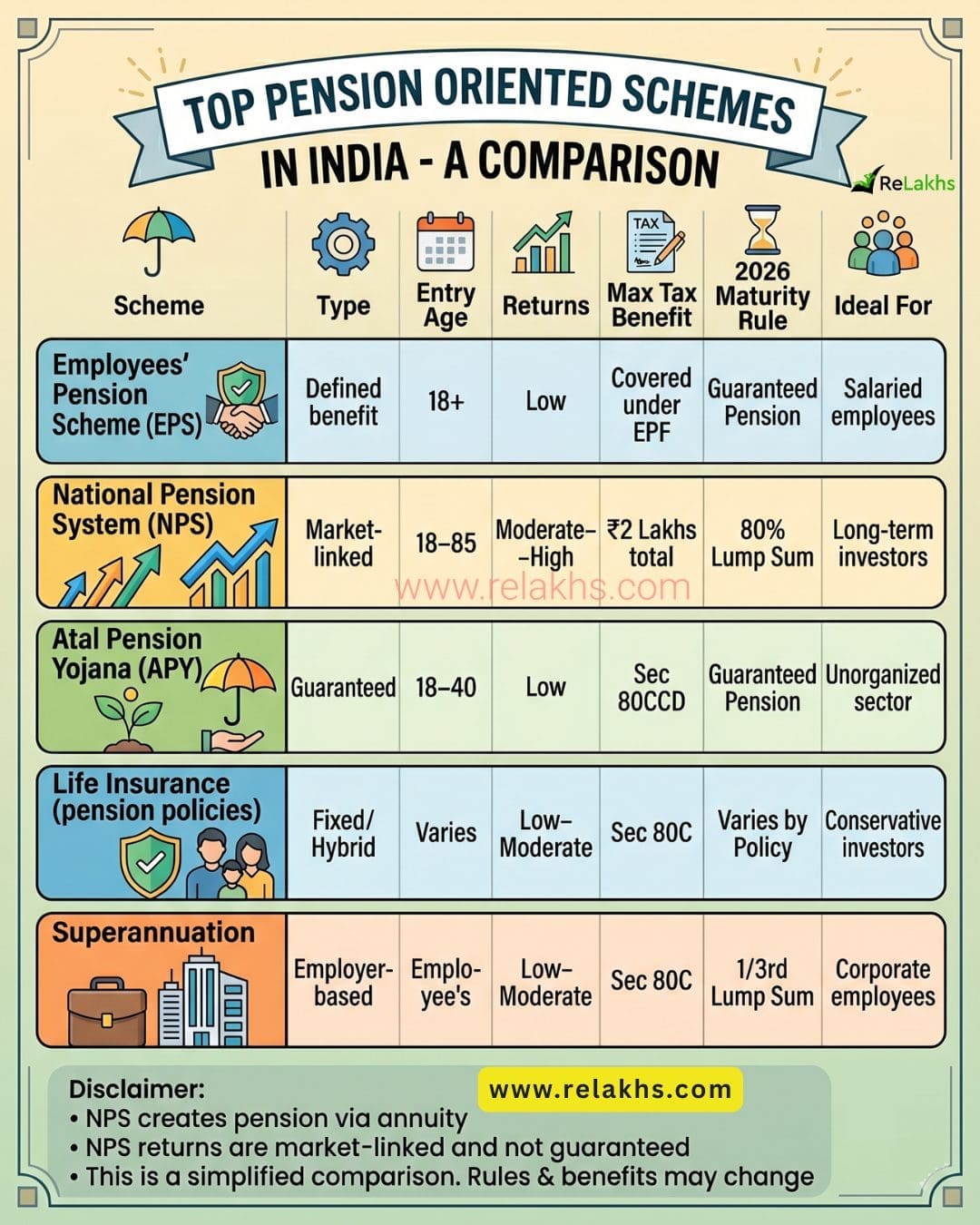

Pension Schemes – Fast Comparability Desk

| Scheme | Sort | Entry Age | Returns | Max Tax Profit | 2026 Maturity Rule | Very best For |

|---|---|---|---|---|---|---|

| EPS | Outlined profit | 18+ | Low | Lined beneath EPF | Assured Pension | Salaried workers |

| NPS | Market-linked | 18–85 | Reasonable–Excessive | ₹2 Lakhs complete | 80% Lump Sum | Lengthy-term buyers |

| APY | Assured | 18–40 | Low | Sec 80CCD | Assured Pension | Unorganized sector |

| Life Insurance coverage | Mounted/Hybrid | Varies | Low–Reasonable | Sec 80C | Varies by Coverage | Conservative buyers |

| Superannuation | Employer-based | Worker | Low–Reasonable | Sec 80C | 1/third Lump Sum | Company workers |

Different Pension-like Earnings Choices

Not Precisely Pension Schemes… However Helpful for Retirement Earnings

These aren’t true pensions (no assured lifelong payout), however they will create regular retirement money move:

- PPF: Tax-free, protected, however 15-year lock-in (extensions potential).

- SCSS: 5%+ curiosity for seniors (60+), 5-year tenure.

- Submit Workplace MIS: 7%+ month-to-month curiosity, low-risk.

- Mutual Fund SWP: Versatile withdrawals from fairness/debt funds (market-linked).

Key distinction: Pensions pay for all times. These have mounted tenures or versatile withdrawals.

“Whereas the above will not be pure pension schemes, they play a vital position in retirement planning. In actuality, a mixture of pension schemes like NPS together with earnings choices like SCSS or SWP can create a steady and inflation-beating retirement earnings.”

Remaining Ideas

No single scheme can deal with your total retirement. A stable retirement plan is all the time a mixture of development, security, and earnings methods.

Probably the most sensible strategy for Indian buyers is to mix:

- NPS for long-term, market-linked development

- EPF/PPF for stability and tax effectivity

- SCSS (post-retirement) for regular earnings

When it comes particularly to pure pension oriented schemes, every serves a distinct objective:

- For development & flexibility: NPS stands out in 2026 resulting from its low value and market-linked returns

- For security & assured earnings: APY and EPS supply predictable pension, although with limitations

- For prime-net-worth people: Life insurance coverage pension plans can present structured, assured annuities together with legacy planning advantages

In the end, there is no such thing as a “one-size-fits-all” resolution. The right combination relies on your age, threat urge for food, earnings stability, and retirement targets. The sooner you propose and diversify throughout these choices, the safer and stress-free your retirement will be.

Proceed studying:

(Submit first printed on : 24-April-2026)