{kind=link}

Most of us continually take a look at “returns” on our investments. However only a few of us take into consideration the actual enemy that quietly eats into these returns – inflation. The logic may be very easy: in case your cash shouldn’t be rising sooner than inflation, you’re really getting poorer yr after yr.

Let me stroll you thru this with a easy, real-life instance.

Take into consideration a easy household dinner at a restaurant. Round 10–12 years in the past, an honest outing for the entire household used to value roughly ₹800–₹1,000. As we speak, the identical form of dinner simply involves ₹4,000–₹5,000 in lots of cities.

Did the amount develop into much more? Did the standard enhance a lot that the soar is totally justified? Probably not.

That is inflation at work.

Costs hold going up over time, and your cash retains shedding its buying energy. ₹100 right this moment won’t purchase you an identical issues 10 or 20 years from now. That’s precisely why inflation is a crucial think about each monetary determination you make.

Why Inflation Is Essential for the Financial system?

Inflation shouldn’t be at all times a villain. The truth is, a average degree of inflation is definitely wholesome for the financial system.

Why? As a result of:

- It nudges folks to spend and make investments as an alternative of simply hoarding money.

- It offers companies room to regularly enhance salaries and develop income.

- It helps help general financial progress.

That’s why central banks just like the RBI intention to maintain inflation at a manageable degree, round 4% (their consolation zone). However at a private degree, inflation can quietly develop into an enormous downside, particularly whenever you’re planning long-term objectives like retirement, youngsters’s training, or shopping for a home.

Why Inflation Issues for People?

For people such as you and me, inflation hits us primarily in 3 ways:

- Buying energy:

- Your cash retains shedding power over time.

- Instance: ₹1 lakh right this moment won’t provide the similar life-style 20 years from now.

- Monetary objectives develop into costlier:

- A objective that prices ₹10 lakh right this moment might value ₹30–₹40 lakh sooner or later, relying on inflation.

- So, should you don’t account for inflation, you’ll severely underestimate how a lot you really want.

- Investments should beat inflation:

- In case your investments are rising at 6% however inflation is 7%, your actual return is unfavourable.

- On paper it appears such as you’re incomes, however in actuality your cash is shedding buying energy.

That’s why inflation is a key enter in each correct monetary plan and objective calculation.

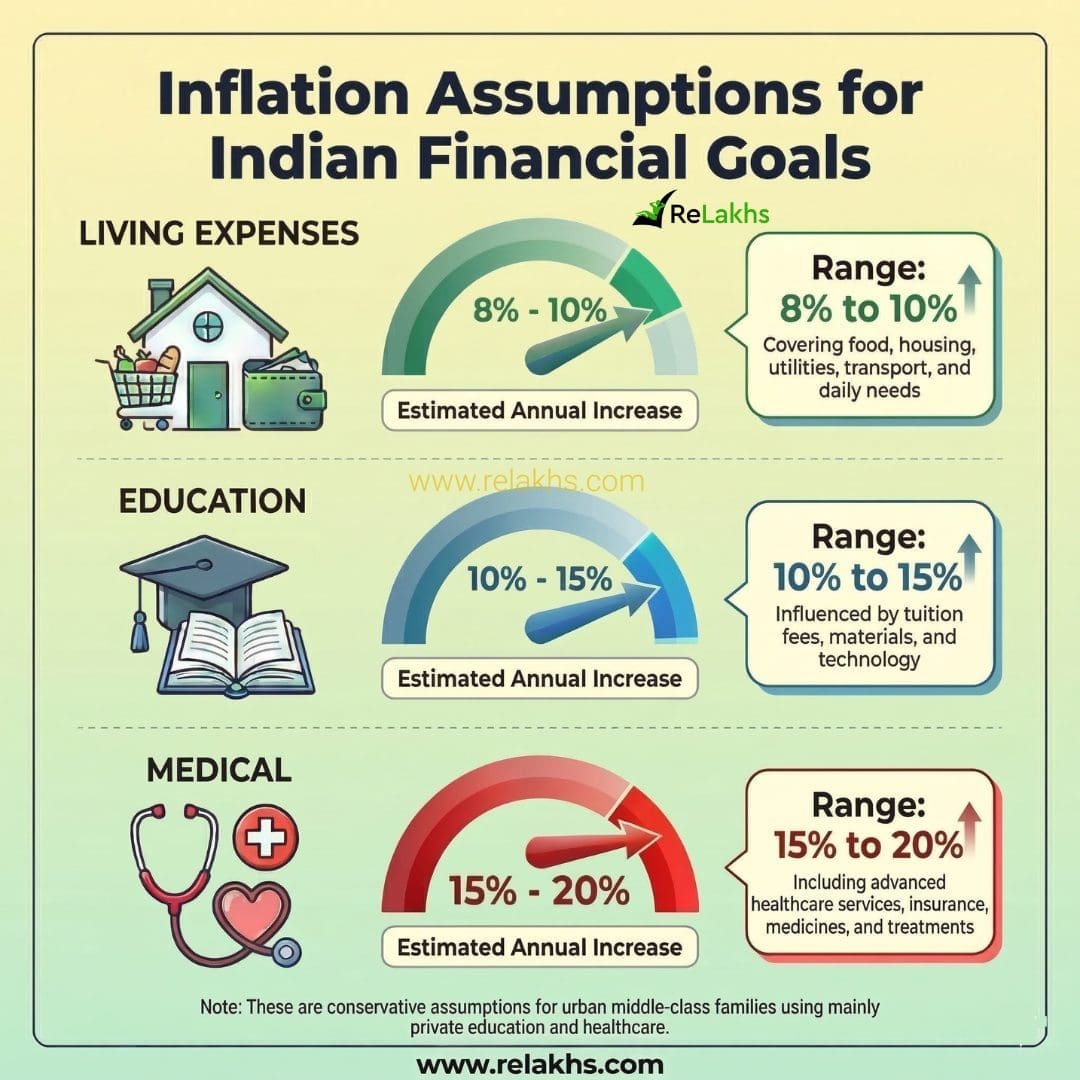

Inflation Assumptions for Monetary Planning in India

Totally different bills develop at completely different inflation charges. Based mostly on long-term developments in India, it’s advisable to imagine the next ranges.

| Monetary Aim | Typical Inflation Vary | Why |

|---|---|---|

| Dwelling Bills | 8% – 10% | Meals, hire, utilities, transport |

| Training | 10% – 15% | Tuition charges, non-public training prices |

| Healthcare | 15% – 20% | Medical therapies, hospital prices, expertise |

A Actual Instance of Training Inflation

Training prices in India are capturing up quick, particularly in non-public faculties and schools.

Take this instance – non-public faculties in Karnataka lately proposed a 15% charge hike for 2025–26, blaming inflation and rising prices. Many already cost ₹50,000–₹75,000 per yr, whereas premium ones simply hit ₹2 lakh+.

That’s why monetary planners use 10–15% training inflation when calculating future prices. Ignore this, and also you’ll severely underestimate how a lot it’s essential save on your youngster’s training.

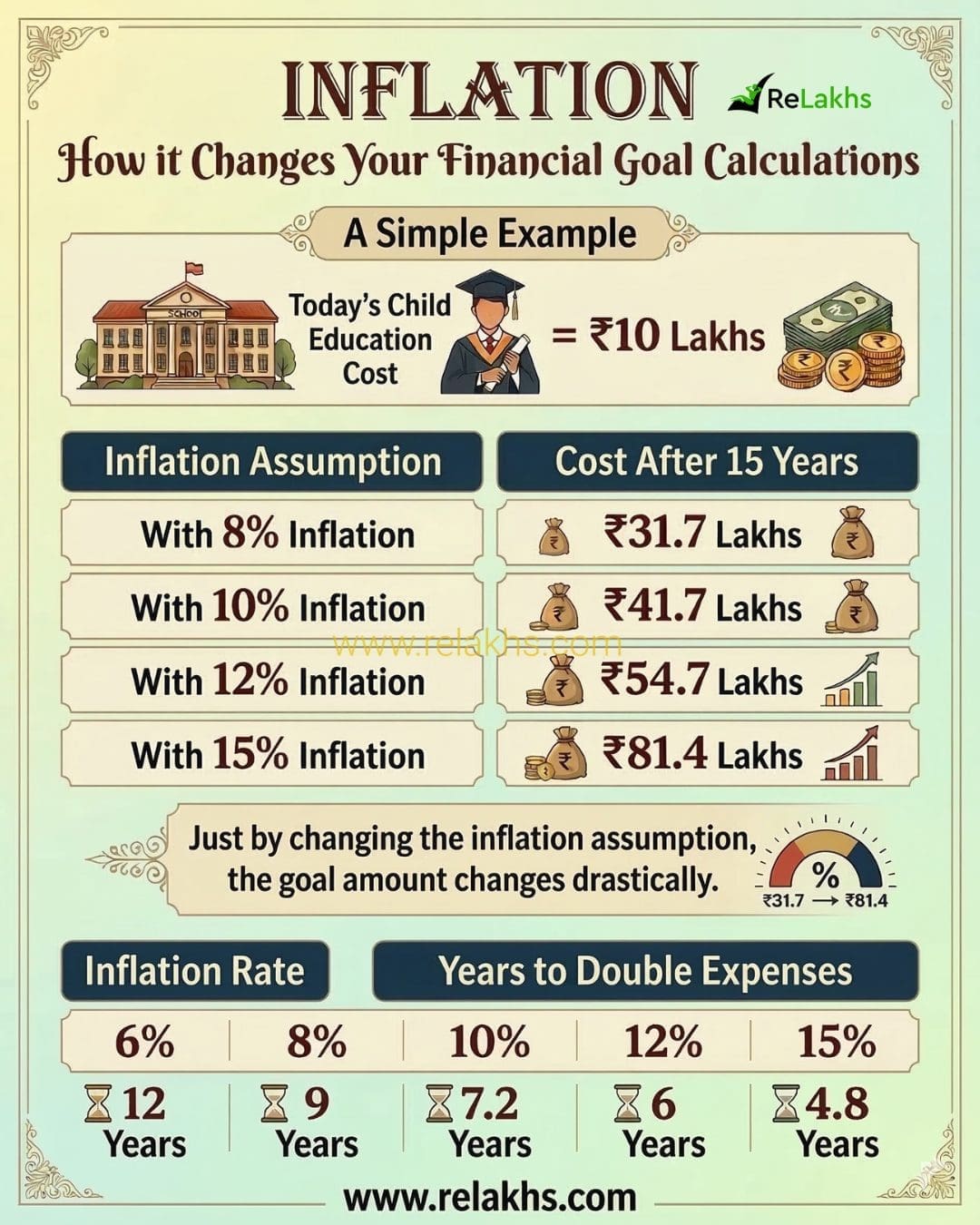

How Inflation Adjustments Your Aim Calculations

Allow us to take a easy instance. Suppose your youngster’s school training prices ₹10 lakh right this moment.

Simply altering the inflation assumption can drastically change the objective quantity. Because of this appropriate inflation assumptions are crucial whereas planning investments.

We will additionally perceive this with a easy rule – The Rule of 72.

Years to double ≈ 72 ÷ Inflation Fee

| Inflation Fee | Years for Bills to Double |

|---|---|

| 6% | 12 years |

| 8% | 9 years |

| 10% | 7.2 years |

| 12% | 6 years |

| 15% | 4.8 years |

• At 10% inflation, your bills double each 7.2 years

• At 15% inflation, they double each 4.8 years

Now think about planning retirement or child’s training with out contemplating this. Your monetary plan might collapse.

Why Inflation Is Essential in Retirement Planning

When planning your retirement corpus, inflation is your silent accomplice you may’t ignore. Give it some thought – should you want ₹50,000 per thirty days right this moment to dwell comfortably, in 20 years that very same life-style may cost ₹1.5–2 lakh after 8–10% inflation.

So, whereas saving, intention for investments that beat inflation constantly (equities, mutual funds usually goal 10–12% returns). Underestimating this implies your retirement nest egg will fall quick, forcing you to chop corners later.

Much more crucial is the withdrawal part.

As soon as retired, inflation doesn’t cease – it retains eroding your corpus. Should you withdraw a hard and fast ₹1 lakh month-to-month with out adjusting, you’ll run out sooner as costs rise. Good planners use a “protected withdrawal charge” of three–4% initially, growing it yearly by inflation (like 6–7%). This fashion, your financial savings final 25–30 years with out depleting.

In monetary planning, ignoring inflation is like constructing a home on weak foundations — it might stand right this moment, however it gained’t final tomorrow.

Key Takeaways

- Inflation silently eats away at your buying energy.

- Each monetary objective wants inflation adjustment in calculations.

- Totally different objectives imply completely different inflation charges.

- In India, typical planning assumptions:

- Dwelling bills → 8–10%

- Training → 10–15%

- Healthcare → 15–20%

- In India, typical planning assumptions:

- Even small inflation variations explode your future objective quantities.

The largest monetary planning mistake? Not low returns — it’s ignoring inflation.

As a result of the actual query shouldn’t be: “How a lot cash will I’ve?”

The true query is: “What is going to that cash have the ability to purchase?”

Proceed studying:

(Publish first printed on : 16-March-2026)