{kind=link}

The cross-border spillover results of shifts in U.S. financial coverage have lengthy been a spotlight of teachers and policymakers alike. A standard discovering within the literature is that adjustments within the stance of U.S. financial coverage have sizable results on financial exercise and monetary markets in rising market economies (EMEs). On this publish, we analyze one particular side of those spillovers: how EMEs fared by the U.S. financial coverage tightening cycle of 2022-23 relative to the predictions of a mannequin, which was calibrated to seize empirically related options of those economies based mostly on historic information. We discover that extra susceptible EMEs fared higher in each monetary market and progress outcomes than can be anticipated from our mannequin, whereas the comparatively much less susceptible fared a bit higher than the mannequin predictions for monetary outcomes however considerably worse for progress outcomes.

The Shift to Tighter U.S. Financial Coverage

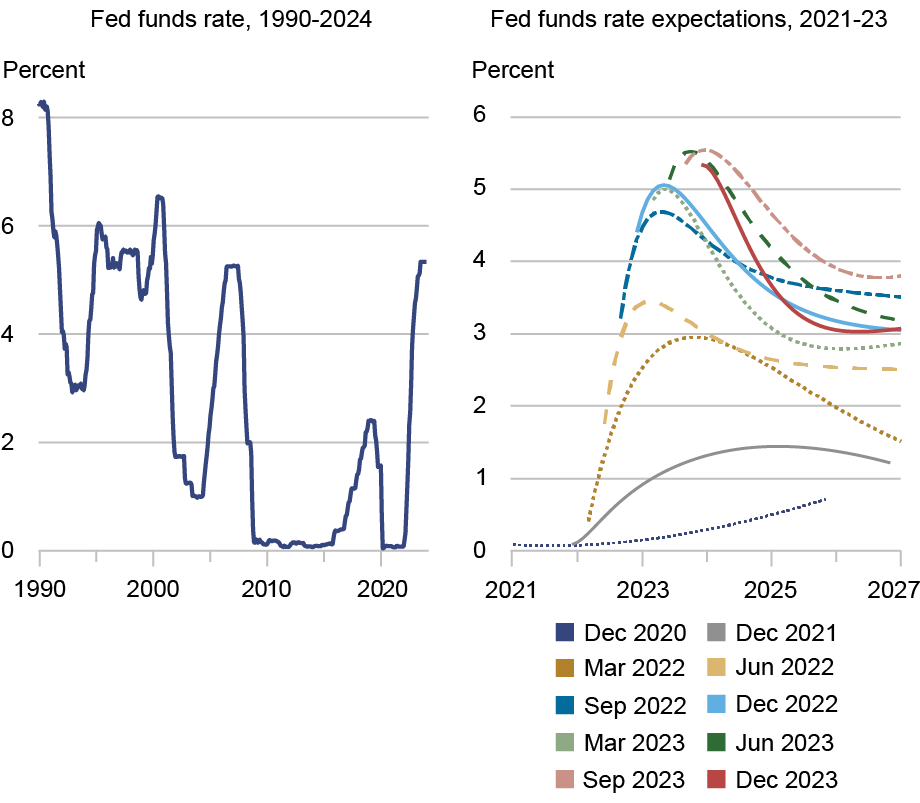

As proven within the left panel of the chart beneath, the latest tightening cycle was unprecedented in each magnitude and velocity, with a cumulative rise within the federal funds fee not seen within the earlier thirty years. The suitable panel of the chart exhibits that market expectations of the fed funds fee path shifted upwards by 4 share factors between late 2021 and late 2023, with the majority of the strikes occurring in 2022. Given the historical past of huge spillovers to EMEs, it is very important know the way resilient these economies have been to this latest aggressive U.S. tightening and the accompanying rise in market expectations of the U.S. coverage fee.

Market Expectations of the Federal Funds Price Path Shifted Upwards by 4 Proportion Factors Between Late 2021 and Late 2023

Notes: The left panel exhibits the extent of the federal funds fee. The suitable panel exhibits market expectations of the long run path of the fed funds fee implied by in a single day curiosity swaps at every of the months indicated within the legend.

Mannequin-Inferred Mixture of Development and Financial Shocks

Our baseline framework is a two-country New Keynesian mannequin consisting of a house nation (a small EME) and the overseas financial system (the US). Right here we current solely a quick overview of our mannequin—full particulars could be present in our latest analysis.

Two of the sources of EME vulnerability play a very necessary position in our evaluation. The primary is the presence of overseas currency-denominated debt in companies’ steadiness sheets, which results in opposed monetary penalties from home forex depreciation that, in precept, can greater than offset the optimistic results by internet exports of such depreciation (modeled as in our earlier analysis). The second is the imperfect anchoring of inflation expectations—a property typical of EMEs with histories of high-inflation episodes and earlier absence of inflation focusing on frameworks. Within the mannequin, we incorporate this function by postulating that companies depend on previous inflation surprises to information their price-setting selections moderately than being fully forward-looking as within the case of well-anchored long-term inflation expectations. It is a easy strategy to seize the concept in some EMEs the central banks’ inflation targets lack full credibility.

Earlier analysis argued that financial tightening has much less opposed penalties when reacting to sturdy combination demand (progress shocks) than heightened inflation pressures (financial shocks). This function displays that U.S. combination demand shocks have optimistic spillovers to different nations that might offset a number of the opposed results from greater U.S. rates of interest.

We use our mannequin to deduce a particular mixture of optimistic progress and opposed financial shocks driving the U.S. tightening, assuming that these two shocks had been the one shocks driving the dynamics of the fed funds fee and U.S. GDP. Right here we use the function that these two shocks would drive U.S. GDP in reverse instructions. Utilizing a measure of the shift in market individuals’ expectations of U.S. progress, together with the shifts within the anticipated path of the fed funds fee proven earlier, we will infer from the mannequin the particular mixture of progress and financial shocks that drove the tightening.

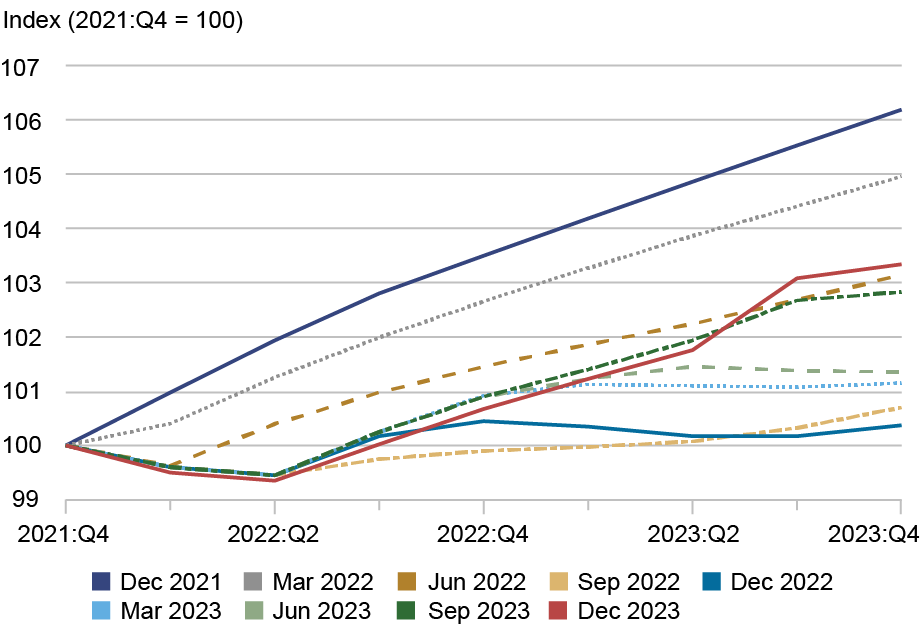

The chart beneath exhibits the evolution of a survey-based measures of U.S. quarterly actual GDP progress expectations of economic analysts, obtained from the Blue Chip Financial Indicators. It exhibits progressive markdowns to anticipated progress by nearly all of 2022 that occurred whereas expectations of the fed funds fee (proven earlier) had been being revised up. This implies that over this era inflation issues had been the dominant issue driving financial coverage, though beginning in December 2022, progress expectations began to be revised upward.

U.S. Actual GDP Expectations Had been Marked Down over A lot of 2022

Predicted vs. Realized Results on Monetary Markets and Actual Exercise

Subsequent, we flip to the query of how the precise evolution of economic variables and actual exercise in much less and extra susceptible rising economies over this tightening interval compares with the mannequin’s predictions for the inferred mixture of progress and financial shocks. EMEs are divided into much less susceptible and extra susceptible teams based mostly on a technique that compares a cross-country vulnerability index introduced on this analysis.

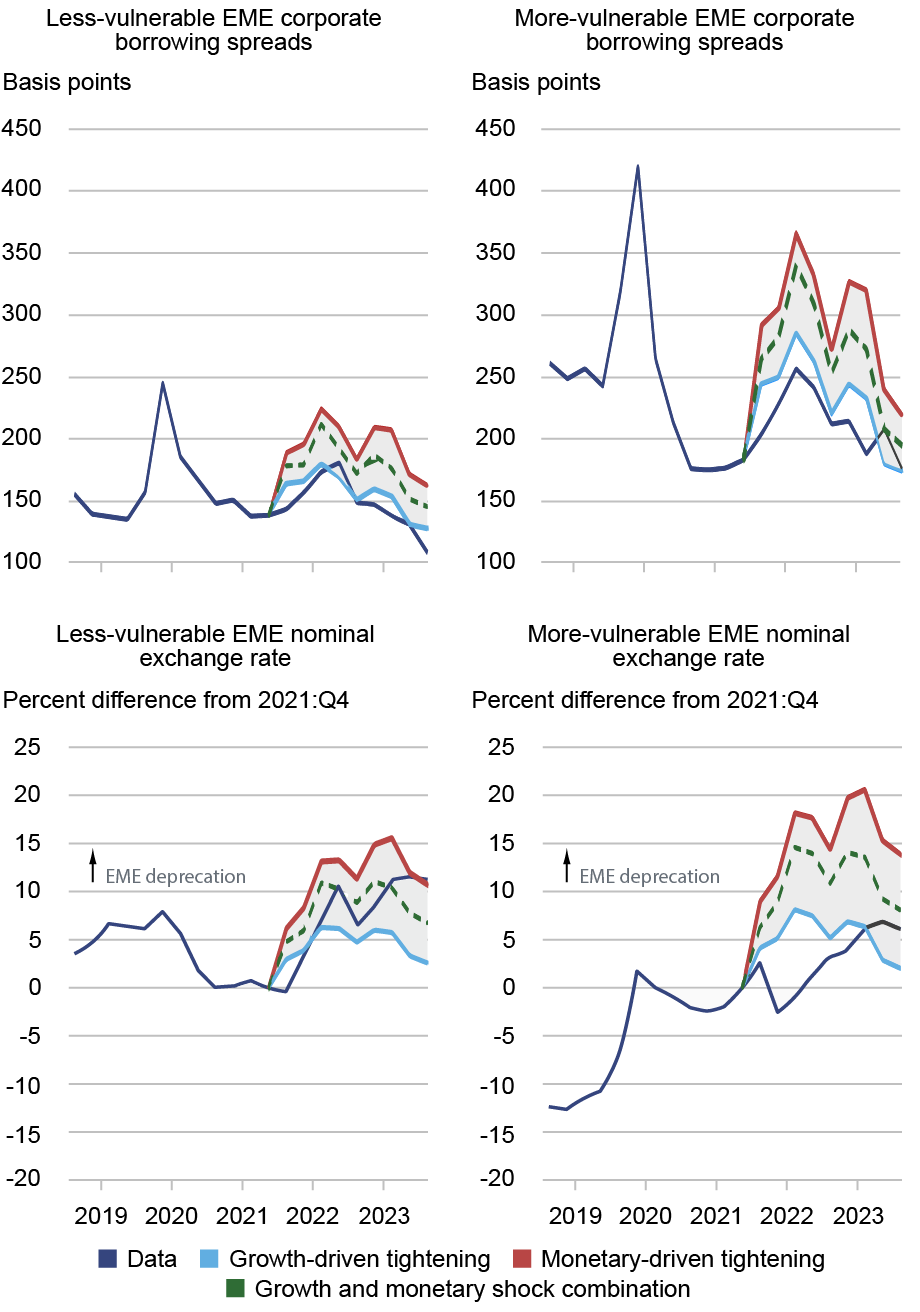

The panel chart beneath exhibits the evolution of EME company borrowing spreads (high row) and EME nominal trade charges (backside row) for much less and extra susceptible EMEs (left and proper columns, respectively). The sunshine blue strains present the mannequin’s predictions when the U.S. tightening is totally growth-driven whereas the crimson strains present the case when it’s utterly monetary-driven. The dashed inexperienced strains present the predictions of the mannequin from the model-inferred mixture of progress and financial shocks. The model-implied paths are constructed by assuming that absent shocks, spreads and trade charges would have remained fixed at their 2021:This autumn ranges. The precise information are proven by the darkish blue strains.

Monetary Spillovers Throughout the Latest U.S. Tightening Cycle Matched Predictions for Much less Susceptible EMEs however Had been Smaller Than Anticipated for Extra Susceptible Ones

Notes: Company borrowing spreads are five-year triple-B company bond spreads issued by firms in Asian EMEs proxying much less susceptible EMEs and by firms in Latin American EMEs proxying for extra susceptible EMEs. The trade fee combination for the much less susceptible EMEs attracts on information for China, Indonesia, Israel, Malaysia, South Korea, Taiwan, Thailand, and Vietnam and for the extra susceptible EMEs on Argentina, Brazil, Chile, Colombia, India, Mexico, Philippines, and Russia. Values are weighted utilizing GDP buying energy parity weights.

For the much less susceptible EMEs, trade charges (backside left panel) behaved largely because the mannequin predicted, exhibiting important depreciations in line with historic patterns. In these similar economies, the extent of company spreads was decrease than what was recommended by the recognized mixture of shocks by the lens of our mannequin, and near the trail implied by assuming progress shocks solely. In distinction, for the extra susceptible economies, the extent of economic stress since early 2022 was significantly decrease than recommended by the growth-monetary shock mixture by the lens of our mannequin, and near the trail implied by assuming progress shocks solely—a situation that signifies they fared higher than anticipated.

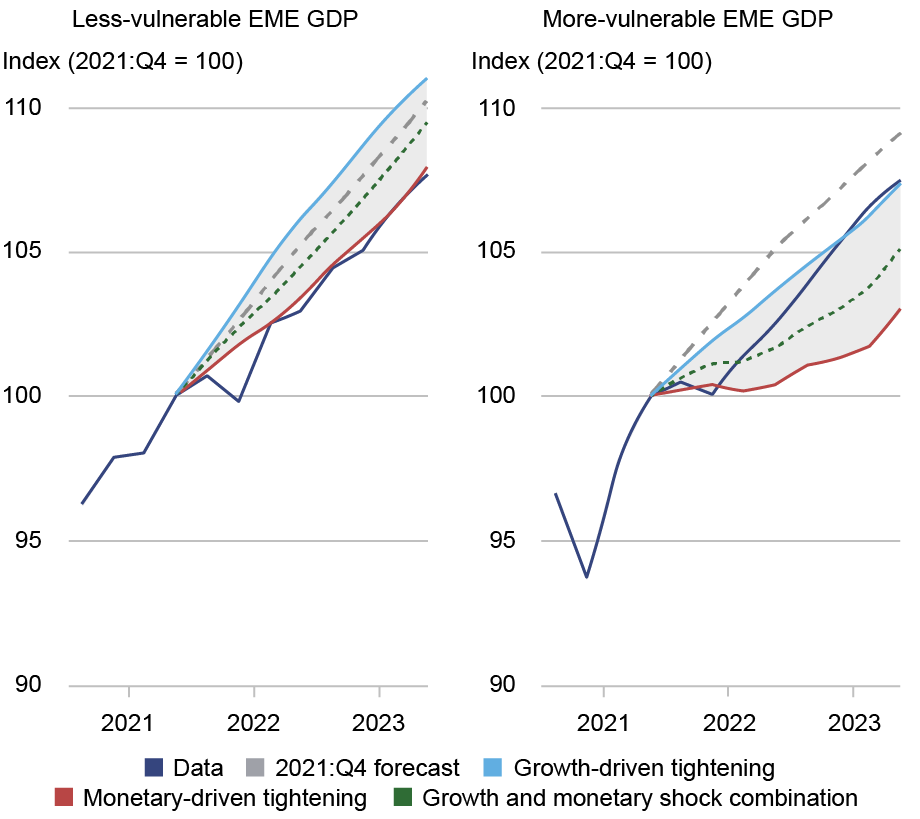

Turning to actual exercise, the message is roughly the identical when trying on the habits of actual GDP ranges, as proven within the chart beneath. Right here the expected outcomes are generated by assuming that absent shocks GDP paths of EMEs would have adopted the trail indicated by non-public sector forecasts as of 2021:This autumn, proven by the dashed-dotted strains. The extra susceptible EMEs (proper panel) displayed outstanding resilience, with GDP ranges significantly greater than the model-implied path from the growth-monetary shock mixture. In distinction, the much less susceptible EMEs (left panel) noticed GDP outcomes effectively beneath these predicted from the growth-monetary shock mixture and really near these implied by assuming monetary-driven tightening solely.

Extra Susceptible EMEs Confirmed GDP Resilience Whereas Much less Susceptible Ones Underperformed Throughout the Latest U.S. Tightening Cycle

Word: Much less and extra susceptible teams are made up of the identical nations as within the trade fee aggregates above.

Total, our proof means that each teams of EMEs fared higher in monetary markets than the mannequin predicted, with extra susceptible economies outperforming by an particularly giant margin. The image for financial exercise was extra blended: extra susceptible economies did significantly higher than predicted, whereas much less susceptible economies did considerably worse.

What May Clarify These Divergent Outcomes?

One attainable interpretation of the divergence in outcomes is that developments outdoors of the US—similar to actions in international commodity costs and China’s progress prospects—affected more-vulnerable and less-vulnerable EMEs otherwise, but these elements aren’t included in our mannequin. Alternatively, extra susceptible EMEs could have strengthened their financial and different coverage frameworks in methods not but mirrored within the vulnerability index variables.

Shaghil Ahmed is deputy director within the Federal Reserve Board’s Division of Worldwide Finance.

Ozge Akinci is head of Worldwide Research within the Federal Reserve Financial institution of New York’s Analysis and Statistics Group.

Albert Queralto is chief of the World Modeling Research Part within the Federal Reserve Board’s Division of Worldwide Finance.

The right way to cite this publish:

Shaghil Ahmed, Ozge Akinci, and Albert Queralto, “How Resilient Had been Rising Market Economies By the 2022‑23 U.S. Financial Tightening Cycle?,” Federal Reserve Financial institution of New York Liberty Avenue Economics, June 26, 2026, https://doi.org/10.59576/lse.20260626

BibTeX: View |

Disclaimer

The views expressed on this publish are these of the writer(s) and don’t essentially replicate the place of the Federal Reserve Financial institution of New York or the Federal Reserve System. Any errors or omissions are the accountability of the writer(s).