{kind=link}

Submit Views:

70

At Truemind Capital, our broad understanding has been:

- The present surroundings requires diversification throughout asset lessons and geographies, as world uncertainties proceed to form market outcomes.

- Investments needs to be guided by valuations and margin of security, guaranteeing draw back dangers stay contained moderately than chasing costly alternatives.

- Asset allocation must be dynamic, with lively rebalancing throughout asset lessons as valuations and alternatives evolve.

- Sustaining liquidity inside portfolios stays important, enabling well timed shifts and efficient deployment throughout market dislocations.

Fairness Market Insights:

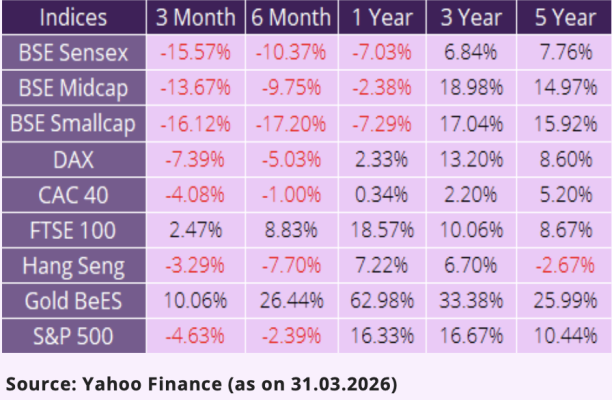

Indian fairness markets remained underneath stress in the course of the January-March 2026 quarter, marking a weak near the monetary 12 months. Benchmark indices ended FY26 in destructive territory, with the BSE Sensex declining round 7% year-on-year, reflecting a broad-based moderation after the robust positive factors seen in earlier years.

Market efficiency in the course of the quarter remained uneven. Whereas large-cap indices confirmed relative resilience, broader markets continued to lag, with mid- and small-cap segments witnessing stress amid stretched valuations and moderating earnings expectations. Participation remained selective, with returns concentrated in restricted pockets moderately than being broad-based.

The ‘Oil & Battle’ Punch: Market sentiment turned bitter in February because the West Asia battle flared up. We noticed Brent crude spike from $72 to over $100 inside weeks. Escalating geopolitical tensions and a pointy rise in world uncertainty have raised considerations about inflation, foreign money stability, and rates of interest within the house turf. This, in flip, weighed on investor confidence and led to elevated volatility throughout fairness markets.

International institutional buyers’ (FIIs) flows additionally weighed on this cautious surroundings. FY26 noticed one of many highest ranges of international outflows, with March alone witnessing outflows of over Rs 1.14 lakh crore (round $12.3 billion) from home equities. Home institutional buyers, nevertheless, continued to supply robust help, partially offsetting the impression of worldwide danger aversion.

Globally, financial progress stays beneath its long-term common because of persistent geopolitical tensions and trade-related uncertainty. Markets seem like coming into a late-cycle section, the place returns are prone to be extra uneven and more and more selective. Whereas liquidity circumstances stay supportive, the effectiveness of liquidity in driving market returns is progressively diminishing.

Wanting forward, company earnings progress is predicted to stay average and uneven. We’re seeing a transparent ‘late-cycle’ shift. Whereas corporations should develop their high traces (revenues), the underside line (income) is being squeezed by rising prices and restricted margin enlargement.

Valuations, whereas corrected from their peaks, are hovering above long-term averages, notably within the broader market segments. Whereas the current correction has improved relative valuations in comparison with rising markets, this doesn’t essentially translate into fast upside, particularly within the absence of robust earnings momentum.

As well as, elevated fiscal deficits throughout main economies, ongoing geopolitical developments, and coverage uncertainties proceed to complicate the worldwide funding surroundings. In such circumstances, robust macro information alone could not translate into broad-based market efficiency.

What we’re doing?

In opposition to this backdrop, we proceed to actively rebalance portfolios in periods of volatility, utilizing short-term debt allocations as a supply of liquidity to deploy into equities at extra affordable valuations. This enables us to keep up alignment with consumer danger profiles whereas tactically adjusting publicity as alternatives emerge.

We proceed to decide on portfolios tilted in the direction of large-cap and value-oriented methods, complemented by selective world publicity for diversification, whereas avoiding aggressive thematic and momentum-driven allocations.

We consider fairness returns over the medium time period are prone to be extra average and earnings-driven, making disciplined portfolio development extra essential than chasing short-term market tendencies.

Debt Market Insights:

Debt markets additionally remained underneath stress throughout this quarter, with yields shifting increased throughout the curve, notably on the lengthy finish. This shift was pushed by a mixture of worldwide and home components, together with elevated crude oil costs and expectations round inflation.

This has been mirrored in authorities bond markets, the place the 10-year G-sec yield moved nearer to the 7% degree, approaching its highest ranges in almost two years. Rising oil costs and foreign money pressures additional added to inflationary considerations, whereas elevated bond provide additionally contributed to upward stress on yields.

From a coverage standpoint, the Reserve Financial institution of India maintained a impartial stance, holding the repo price unchanged at 5.25% and has revised its GDP estimates marginally downward for Q1/Q2FY27 to six.8% and 6.7%, respectively. In our view, the present price surroundings suggests restricted room for additional price cuts within the close to time period. The trajectory of rates of interest will largely rely on how inflation evolves, notably in mild of sustained power worth pressures, and the extent to which progress is impacted over the approaching quarters.

As yields have moved increased, bond costs have adjusted accordingly, resulting in mark-to-market stress, notably in longer-duration devices. This dynamic has been seen throughout debt mutual fund classes, the place longer-duration funds have seen extra volatility in comparison with shorter-duration segments.

On the identical time, the rise in yields has improved the general carry accessible in fixed-income markets. With yields at comparatively increased ranges, buyers are capable of lock in additional enticing accrual alternatives, notably in shorter-duration devices.

Our Strategy to Debt Allocation

At Truemind, we proceed to view debt as a stabilising element of portfolios moderately than a supply of return maximisation. Given the present surroundings, we keep our choice for shorter-duration and high-quality accrual methods, the place the risk-reward profile stays extra beneficial. These segments provide higher visibility of returns whereas limiting publicity to rate of interest volatility as in comparison with longer-duration exposures.

We additionally proceed to utilise arbitrage funds and short-term debt devices as a part of portfolio development, notably for managing liquidity and enhancing post-tax effectivity.

Because the rate of interest cycle evolves, alternatives in period could emerge. Nevertheless, at current, sustaining a disciplined and selective strategy stays key to navigating the mounted earnings investments.

Different Asset Lessons:

Gold too witnessed a unstable section in the course of the current interval, with costs shifting in each instructions moderately than following a transparent upward development. Whereas world uncertainties and geopolitical tensions usually help gold costs, the current interval noticed intermittent corrections pushed by revenue reserving and liquidity wants.

That stated, gold continues to play an essential function as a portfolio diversifier, notably in intervals of elevated world uncertainty. Nevertheless, its short-term actions could stay influenced by a mixture of things, together with world liquidity, foreign money actions, and investor positioning.

The actual property sector continues to indicate a combined development. Whereas residential costs have remained agency, notably in premium segments, demand has been more and more selective throughout markets.

Latest information exhibits moderation in exercise, whereby housing gross sales declined on a quarter-on-quarter foundation amid world uncertainties, at the same time as long-term demand stays resilient. Progress continues to be concentrated in higher-ticket segments, whereas affordability constraints and cautious sentiment have weighed on broader participation. Given its cyclical nature, illiquidity, and evolving demand dynamics, actual property needs to be seen as a complementary asset inside a well-diversified portfolio.

Truemind’s Mannequin Portfolio – Present Asset Allocation

Private Finance Capsule:

Funding Influence of Battle

Easy methods to survive your funds in International uncertainty?

For any question or dialogue, you will get in contact right here: https://www.truemindcapital.com/contact-us