{kind=link}

On February 26, 2026, the Securities and Alternate Board of India (SEBI) launched main mutual fund reforms to make sure schemes stay “true to label.” The brand new guidelines embody the launch of Life Cycle Funds, discontinuation of Resolution-Oriented schemes, the next 80% minimal fairness requirement for choose classes, stricter portfolio overlap limits, and a phased implementation timeline via 2026–2029.

Not dramatic.

Not sensational.

However structurally necessary.

For those who look intently, this round isn’t about introducing new merchandise—it’s about correcting course. Over time, the boundaries between fund classes started to blur, and names steadily became advertising labels somewhat than true reflections of technique. Some so-called “fairness” funds quietly decreased their fairness publicity, whereas sure “solution-oriented” funds morphed into little greater than static hybrids.

SEBI’s new transfer is basically an try to revive that misplaced alignment and convey readability again to fund classifications. For those who put money into mutual funds — or plan to — this replace straight impacts you.

Let’s break it down in easy phrases.

SEBI 2026 Mutual Fund Guidelines & Reforms

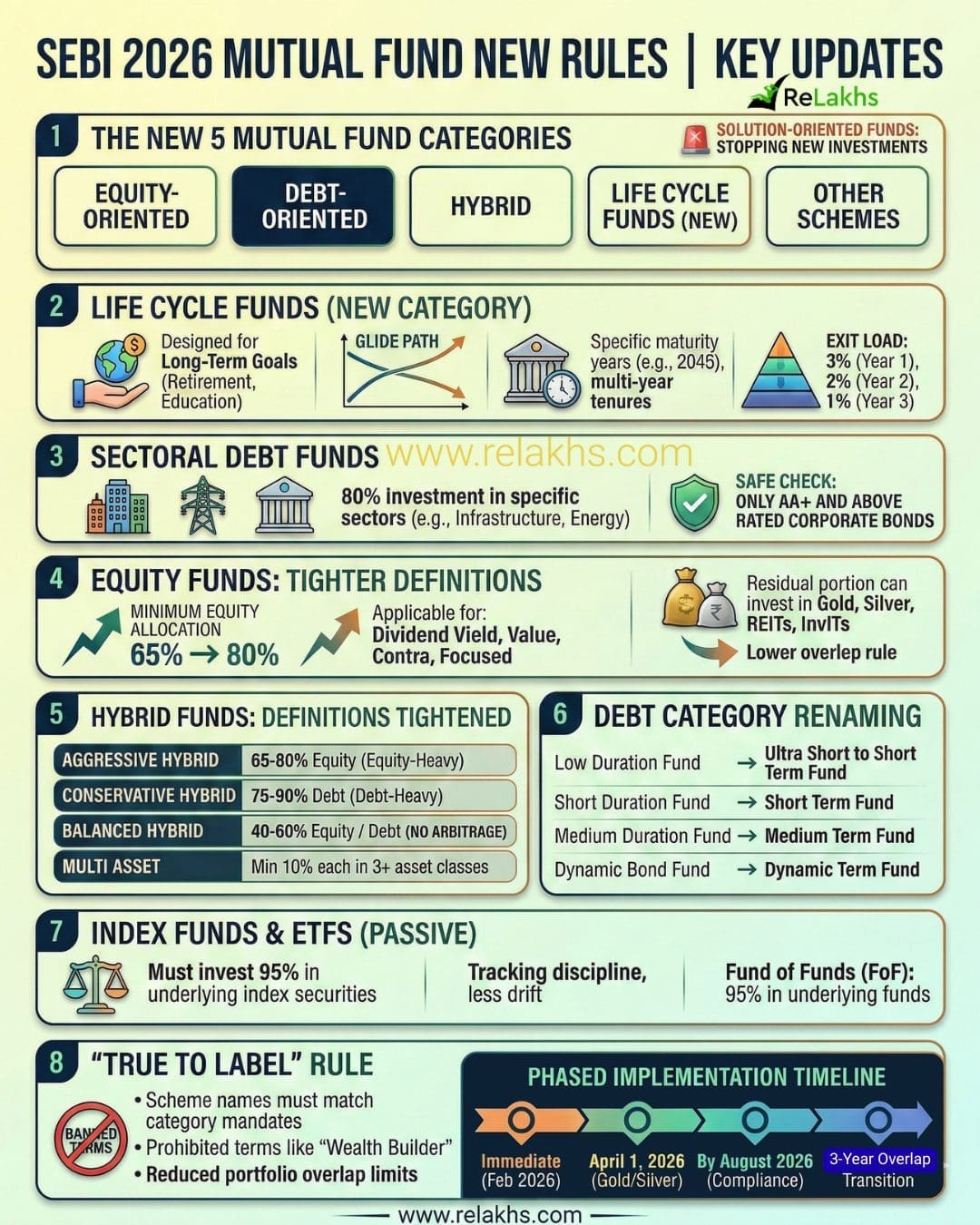

1. The New 5 Broad Mutual Fund Classes (2026 Framework)

SEBI has now grouped all mutual fund schemes beneath 5 main buckets:

- Fairness-Oriented Schemes

- Debt-Oriented Schemes

- Hybrid Schemes

- Life Cycle Funds (New)

- Different Schemes (Index Funds, ETFs, Fund of Funds)

The most important change is in two elements: SEBI is bringing in Life Cycle Funds and shutting down Resolution-Oriented Funds.

Resolution-Oriented schemes like retirement and kids’s funds will not be allowed to take new cash (recent investments) and can finally be merged into different funds with an analogous asset combine and threat stage. For those who’re invested in a retirement fund, you can not high up now. Your AMC will contact you relating to the transition.

2. Life Cycle Funds: New Fund Class

It is a fully new class. As per SEBI, these funds are designed for long-term targets like retirement or youngsters’s training.

- Traits: These funds comply with a glide path, beginning with excessive fairness publicity and steadily shifting to safer belongings (debt/gold) because the goal maturity date approaches.

- Maturity: Launched with particular goal years (e.g., “Life Cycle Fund 2045”) in tenures of 5 to 30 years (multiples of 5).

- Exit Load: To encourage self-discipline, a tiered exit load applies (3% in 12 months 1, 2% in 12 months 2, and 1% in 12 months 3).

| Function | Guideline |

|---|---|

| Tenure | 5, 10, 15, 20, 25, 30 years |

| Naming | Should embody maturity yr (e.g., “Life Cycle Fund 2045”) |

| Asset Combine | Fairness + Debt + Gold/Silver ETFs + InvITs |

| Exit Load | 3% (12 months 1), 2% (12 months 2), 1% (12 months 3) |

My Tackle Life Cycle Funds: When Securities and Alternate Board of India (SEBI) launched Life Cycle Funds, the intent was self-discipline and ease. However suitability relies on the investor.

- Pre-defined glide path – The fund reduces fairness routinely over time. Your life, revenue, and threat urge for food could not comply with that fastened schedule.

- Much less flexibility – Tiered exit hundreds (3%–2%–1%) encourage self-discipline, however additionally they make early changes pricey in case your targets change.

- Might duplicate your allocation – For those who already handle fairness, debt, and gold individually, a Life Cycle Fund might merely bundle what you’re already doing — with much less management.

- Automation vs management – Useful for buyers who battle with rebalancing; pointless for these snug managing asset allocation themselves.

- Construction ≠ suitability – Simply because it’s goal-based and structured doesn’t imply it suits each monetary journey.

- Life Cycle Funds aren’t inherently “good” or “unhealthy.” They’re extremely structured by design. And that construction shines brightest for the correct of investor.

3.Sectoral Debt Funds Launched

That is one other new class. These funds can now make investments 80% in debt devices of a selected sector, comparable to:

- Infrastructure

- Vitality

- Monetary Companies

There’s additionally a security filter: these funds can make investments solely in company bonds rated AA+ and above, which improves readability for buyers and helps preserve a examine on extreme credit score threat.

4.Fairness Funds: Tighter Definitions

That is the place many buyers may even see adjustments. Minimal fairness allocation for a number of classes has been raised from 65% to 80%, together with:

- Dividend Yield Funds

- Worth Funds

- Contra Funds

- Centered Funds

On the similar time, fairness funds can now use gold, silver, REITs and InvITs of their residual portion.

Earlier, AMCs had to decide on between providing both a Worth Fund or a Contra Fund. Now they will launch each, however with a strict restrict—the portfolio overlap between them can’t exceed 50%. This transformation encourages extra choices whereas stopping extreme similarity between the schemes.

5.Hybrid Funds: Definitions Tightened

SEBI has additionally refined hybrid classes.

One key change: Arbitrage is NOT allowed in Balanced Hybrid Funds anymore. This prevents misuse of the class purely for tax effectivity.

| Class | Fairness | Debt | Notes |

|---|---|---|---|

| Conservative Hybrid | 10–25% | 75–90% | Debt-heavy |

| Balanced Hybrid | 40–60% | 40–60% | No arbitrage |

| Aggressive Hybrid | 65–80% | 20–35% | Fairness-heavy |

| Multi Asset | Min 10% every | Min 10% every | At the least 3 asset lessons |

6.Debt Class Renaming (Readability Transfer)

A number of debt fund classes have been renamed for readability:

| Previous Identify | New Identify |

|---|---|

| Low Period Fund | Extremely Brief to Brief Time period Fund |

| Brief Period Fund | Brief Time period Fund |

| Medium Period Fund | Medium Time period Fund |

| Dynamic Bond Fund | Dynamic Time period Fund |

7.Index Funds, ETFs & Arbitrage Funds

As per the 2026 reforms by Securities and Alternate Board of India (SEBI):

- Index Funds & ETFs should make investments not less than 95% within the securities of the index they observe.

- Fund of Funds (FoF) should make investments 95% of their underlying fund(s).

At first look, this appears like a small technical element. In passive investing, consistency issues greater than creativity. An index fund ought to behave just like the index — not like an lively fund with money positions.

The 95% rule cuts down on drift by implementing higher monitoring self-discipline and limiting pointless deviations. It quietly reinforces the core precept of staying true to the fund’s label.

SEBI pointers now require Arbitrage Funds to take a position their non-equity portion primarily in Authorities Securities (G-Secs) with a maturity of as much as 1 yr. This shift prioritizes security and liquidity whereas curbing credit score threat in these equity-oriented schemes.

8. “True to Label” – The Huge Rule

That is the philosophical core of the reform.

- Strict Naming Guidelines: SEBI has launched strict naming guidelines the place scheme names should precisely match their class names, leaving no room for artistic advertising spin.

- Banned Deceptive Phrases: Phrases like “Wealth Builder,” “Excessive Progress,” or “Energy Features” are actually prohibited from fund names. The identify should clearly replicate the fund’s precise mandate and technique.

- Portfolio Overlap Limits: Sectoral and thematic funds now face restrictions the place portfolio overlap with different schemes from the identical AMC can’t exceed 50% (excluding large-cap funds). This ensures higher differentiation and transparency throughout choices.

My Take:

When SEBI talked about “True to Label,” it may need sounded technical at first. However the concept is definitely quite simple. If a fund calls itself a Worth Fund, it ought to make investments like one. If it’s labeled a Balanced Fund, it ought to genuinely keep balanced.

The identify should replicate the fund’s precise technique—not simply advertising hype. Many buyers choose funds based mostly on these class names with out digging into month-to-month portfolios.

So when labels drift from actuality, they find yourself carrying hidden dangers. “True to Label” isn’t about chasing increased returns. It’s about restoring honesty to classifications. Not a flashy reform, however a vital one.

SEBI 2026 Mutual Fund New Guidelines: Timeline

- Speedy (Feb 26, 2026):

- Resolution-Oriented funds stopped recent subscriptions.

- AMCs can launch Life Cycle & Sectoral Debt funds.

- By August 2026 (6 Months):

- All schemes should align names.

- Fairness flooring have to be elevated to 80% the place required.

- Month-to-month portfolio overlap stories have to be printed.

- Particular Timeline:

- Gold & silver valuation adjustments efficient April 1, 2026. (From April 1, 2026, gold and silver holdings will comply with a revised home spot-price valuation methodology.)

- Sectoral and thematic funds have a three-year phased timeline (35% + 35% + 30%) to scale back extra portfolio overlap.

| Part | Efficient Date | What Modifications |

|---|---|---|

| Speedy Impact | February 26, 2026 | • Resolution-Oriented schemes cease recent subscriptions • AMCs allowed to launch Life Cycle Funds & Sectoral Debt Funds |

| Gold & Silver Valuation Replace | April 1, 2026 | • Bodily gold & silver to be valued based mostly on revised home spot-price methodology |

| 6-Month Compliance Window | By August 2026 | • True-to-label naming alignment • Fairness flooring improve (65% → 80%) the place relevant • Portfolio realignment• Month-to-month portfolio overlap disclosures |

| Portfolio Overlap Transition (Sectoral/Thematic Funds) | 3-12 months Phased Discount | • 12 months 1: Take away 35% of extra overlap • 12 months 2: Take away further 35% • 12 months 3: Take away remaining 30% |

What Ought to Traders Do?

For those who’re a mutual fund investor:

- Don’t panic.

- Your present items are secure.

- Look ahead to communication out of your AMC.

- Re-evaluate your allocation in case your fund adjustments class or threat stage.

For those who’re holding a Retirement/Youngsters’s fund: You can not add recent cash. Watch for the merger particulars earlier than taking motion.

In markets, drift occurs steadily. Classes stretch, definitions blur, and advertising typically drowns out the precise mandate. Each few years, a reset turns into important. This 2026 reform seems like precisely that—a corrective step somewhat than a revolution. For buyers, that readability is often much more priceless than added complexity.

Proceed studying:

(Publish first printed on : 01-Mar-2026)