{kind=link}

Firm Overview

Omnitech Engineering Restricted is a producer of high-precision engineered parts and assemblies provided to unique tools producers (OEMs) throughout vitality, industrial tools, and movement management and automation sectors. The corporate operates a build-to-specification manufacturing mannequin, producing customised machined parts and assemblies for integration into industrial equipment and safety-critical purposes. As of September 30, 2025, the corporate had serviced over 256 clients throughout 24 nations, primarily serving clients in North America and Europe.

Objects of the provide

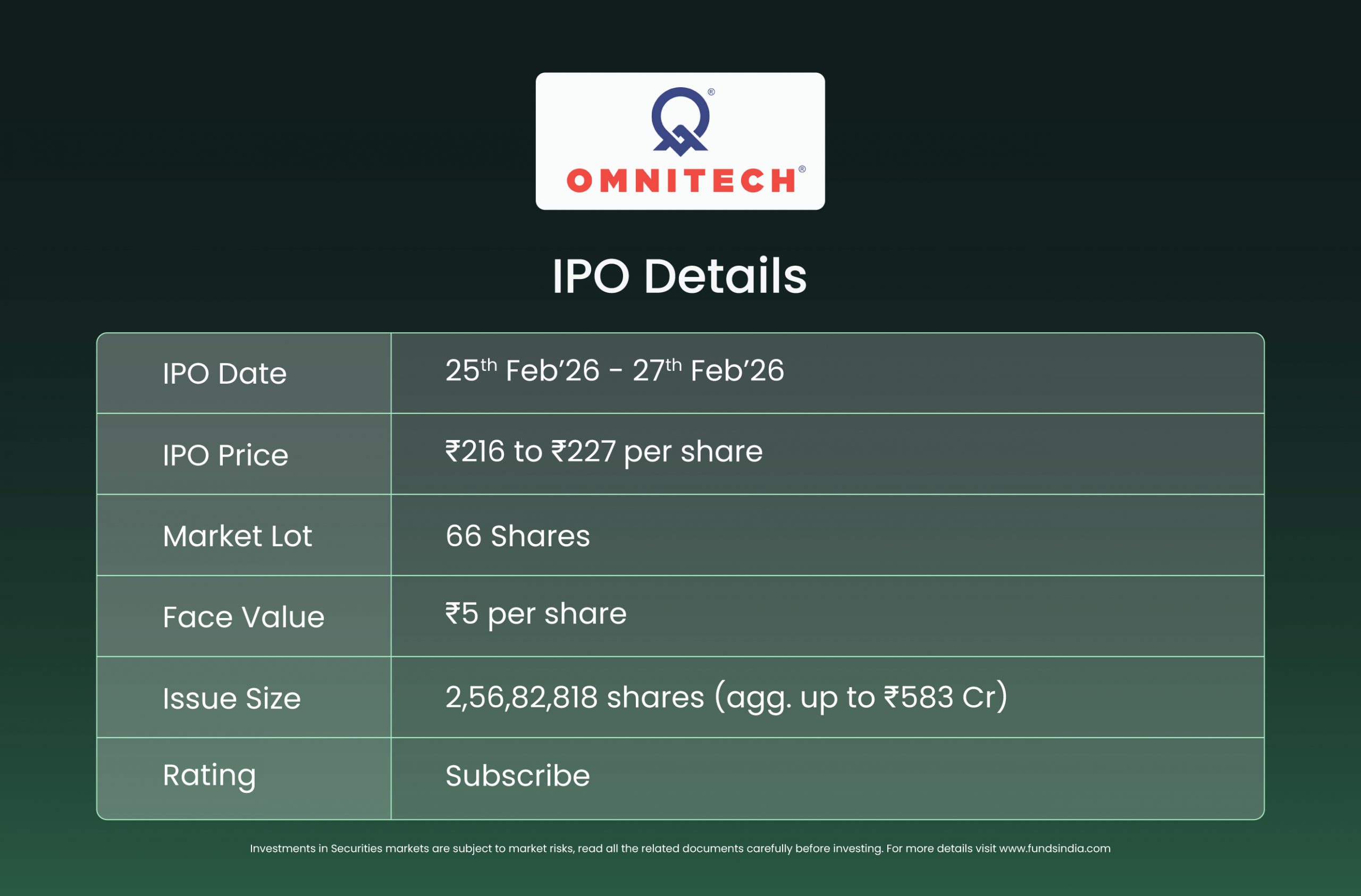

The corporate is finishing up a book-built problem of Fairness Shares of face worth of Rs. 5 every aggregating as much as Rs. 583 crore, comprising a Contemporary Subject aggregating as much as Rs. 418 crore by the Firm and an Provide for Sale aggregating as much as Rs. 165 crore by the Promoting Shareholders.

The proceeds of the recent problem are to be utilized in direction of the next objects:

- Reimbursement and / or pre-payment, in full or partially, of sure excellent borrowings of the corporate.

- Organising new manufacturing services in Rajkot, Gujarat

- Funding capital expenditure in direction of set up of rooftop photo voltaic panels and buy of kit and equipment at current manufacturing services.

- Normal company functions.

Funding Rationale

- Buyer stickiness pushed by qualification-intensive outsourcing mannequin – Omnitech operates inside precision engineered parts manufacturing, the place provider onboarding includes prolonged qualification and validation processes earlier than business provide begins. The corporate holds trade certifications together with API Spec Q1, API 7-1 and API 5CT, enabling provide of parts utilized in safety-critical vitality purposes and forming a key prerequisite for vendor approval by world OEM clients. This creates structurally sticky buyer relationships as soon as approvals are secured. Repeat clients contributed 96.87% of income for the six months ended September 30, 2025, reflecting continued order stream from established OEM relationships. The corporate has provided merchandise to over 256 clients throughout 24 nations, primarily servicing world OEMs in vitality and industrial tools purposes, the place switching suppliers usually requires requalification and operational revalidation, supporting continuity of demand.

- Export-driven income profile linked to world industrial capex cycles – The corporate derives a majority of its income from exports (~79% of income was derived from outdoors India in H1FY26), linking efficiency to world industrial and vitality capital expenditure cycles moderately than home demand circumstances. The worldwide precision engineered items market was valued at USD 269.1 billion in CY2024 and is predicted to develop at a 9.9% CAGR throughout CY2025–CY2028. Participation in world OEM provide chains positions the corporate to learn from ongoing outsourcing developments for specialised precision manufacturing capabilities, and provide chain diversification initiatives (China +1).

- Giant order guide offering income visibility – As of September 30, 2025, the corporate reported an order guide of Rs. 1,764.7 crore, representing roughly 551% of annualised income. The order guide is predominantly pushed by the vitality section (74%), adopted by industrial tools programs (21%) and movement management and automation (3.7%). Publicity to long-cycle industrial and vitality tools packages offers ahead visibility, as manufacturing schedules and procurement timelines usually prolong throughout a number of reporting durations.

- Operational scale and utilisation – Omnitech’s operational profile displays established execution functionality supported by scaled manufacturing infrastructure and steady capability utilisation. As of September 30, 2025, the corporate operated three manufacturing services with annualised machining capability of 24,29,856 machine hours, working at utilisation of ~73% throughout H1FY26, and an annualized fabrication capability of seven,200MTPA. The operational base is supported by a workforce of 1,807 workers, together with devoted manufacturing and high quality groups, enabling end-to-end execution throughout machining, fabrication, meeting and testing processes.

- Monetary Efficiency – The corporate reported consolidated income from operations of Rs. 342.9 crore in FY25, reflecting a 92.45% YoY improve from Rs. 178.1 crore in FY24. EBITDA stood at Rs. 117.6 crore in FY25, with an EBITDA margin of 34.31%, in contrast with Rs. 64.9 crore (36.44% margin) in FY24, representing an 81.2% YoY progress. Revenue after tax (PAT) for FY25 was Rs. 43.9 crore, rising 131.9% YoY from Rs. 18.9 crore in FY24. PAT margin expanded 215 bps to 12.54% in FY25. For H1FY26, the corporate recorded income from operations of Rs. 228 crore, EBITDA of Rs. 70.1 crore, and PAT of Rs. 27.8 crore, with EBITDA margin and PAT margin at 30.72% and 11.74%, respectively.

Key Dangers

- Working capital intensive operations and money stream dependence – The corporate operates a working capital-intensive enterprise mannequin, with internet working capital days at ~282 days in FY25, pushed by elevated stock and receivable cycles typical of precision engineering outsourcing. Lengthy manufacturing lead occasions, prolonged credit score phrases, and comparatively decrease bargaining energy with suppliers, lead to a chronic money conversion cycle the place the corporate successfully funds each manufacturing and buyer credit score concurrently. The elevated working capital requirement represents a structural function of the enterprise mannequin, and sustained progress could due to this fact require continued reliance on prudent working capital administration, and exterior working capital financing.

- Buyer focus danger – The corporate derives a good portion of its income from a concentrated buyer base, with the highest 10 clients contributing between ~48% and ~69% of income throughout latest durations. The enterprise mannequin depends on long-term provide relationships with world OEM clients, and whereas qualification processes create switching prices, dependence on a restricted variety of clients exposes the corporate to demand volatility within the occasion of order reductions, program delays or lack of key buyer relationships.

- Operational execution danger linked to customised manufacturing mannequin – The corporate operates underneath a build-to-specification manufacturing mannequin, the place manufacturing is undertaken in opposition to customer-specific designs and income recognition is determined by profitable execution, inspection and buyer acceptance. Elements are sometimes utilized in safety-critical purposes requiring stringent high quality validation and adherence to express specs. Delays in manufacturing, high quality deviations or prolonged buyer approval cycles could defer income recognition and lengthen working capital cycles. Given the personalised nature of manufacturing, stock and work-in-progress could have restricted alternate use.

Outlook

The corporate’s outlook is supported by a powerful order pipeline, ongoing capability enlargement and sustained demand from world OEM clients, with positioning in safety-critical purposes and certification-led entry boundaries supporting continuity of orders. Progress will rely upon profitable execution throughout customised manufacturing packages and efficient absorption of incremental capability. Whereas the enterprise carries structurally excessive working capital necessities and execution dependence inherent to precision engineering outsourcing, these mirror working traits of the mannequin moderately than structural weaknesses, with efficiency contingent on disciplined working capital administration and constant supply execution as scale will increase.

Based on the RHP, the corporate’s listed friends are PTC Industries Ltd, MTAR Applied sciences Ltd, Dynamatic Applied sciences Ltd, and Azad Engineering Ltd, amongst others. The peer group is buying and selling at a median P/E of 184.9x, with the best being 428.48x, and the bottom being 56.68x. On the higher worth band, the itemizing market capitalization of Omnitech will probably be Rs. ~2,807 crore, and the corporate is demanding a P/E of ~63.94x, primarily based on the put up problem market capitalization and FY25 diluted EPS. When in comparison with its friends, the difficulty appears to be pretty valued. Based mostly on the above views, we offer a ‘Subscribe’ ranking for this IPO.

Disclaimer: Investments within the securities market are topic to market dangers, learn all associated paperwork rigorously earlier than investing. Securities quoted listed here are exemplary, not recommendatory. Please seek the advice of your monetary advisor earlier than investing. Please word that we don’t assure any assured returns for the securities quoted right here.

Analysis disclaimer: Funding within the securities market is topic to market dangers. Learn all of the associated paperwork rigorously earlier than investing. Registration granted by SEBI, and certification from NISM by no means assure the efficiency of the middleman or present any assurance of returns to buyers.

For extra particulars, please learn the disclaimer.

Different articles chances are you’ll like

Put up Views:

147